Contributing Editor

Peanut producers experienced an unusually rough start in getting the crop in the ground. In the Southeast, dry and relatively cool temperatures caused peanuts to emerge slowly. One Extension specialist says that the lack of heat units in the early season has the 2023 crop seven to 10 days behind. In Georgia, wet soils caused the seed to rot and not germinate properly. One farmer replanted more than 1,000 acres. Seed vigor was cited as a major culprit.

A Contract Disconnect

The peanut market has been trending higher as farm leaders try to convince policy makers that inflation and increased costs of production strongly encourage producers to consider other crops. In isolated cases, some farms are not planting any crop at all because of costs. There is definitely a disconnect between what is being offered for farmer stock and what a grower is willing to sign a contract for at this time.  Some producers are even waiting until harvest, or at least during the growing season, to do their contracting. Corn and cotton prices have offered no excitement, either.

Some producers are even waiting until harvest, or at least during the growing season, to do their contracting. Corn and cotton prices have offered no excitement, either.

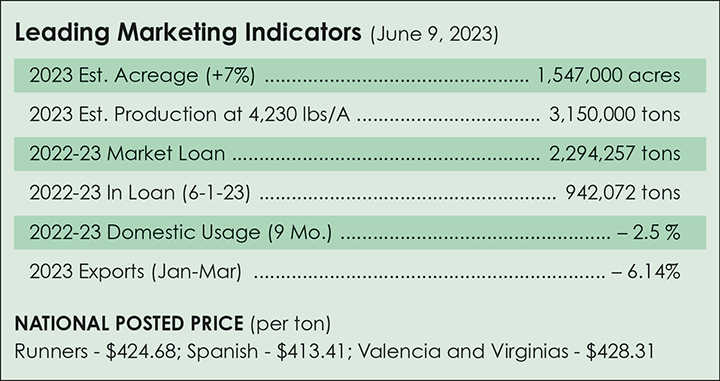

Producers figure that the 2.7 million-ton crop this past year and the 18% plus increased costs of production merited a higher offer for 2023 contracts. In Washington D.C., an ag economist testified that the cost of production in 2022 was approximately $668 per ton. With acreage estimates up 7% or more, shellers started offering $500 to $525 per ton for runner-type peanuts, $525 per ton on high-oleic crop and $550 to $575 per ton on Virginia type. Some shellers offered a sheller pool with a $500 per-ton floor hoping for prices to increase later this season. Prices were higher for Southwest varieties because of the cost of production on irrigated peanuts.

Markets A Bit Firmer

The market reports that there was a lot of new crop business done in late April/early May, and shellers are comfortable. Officials believe that what has been contracted has been sold, and farmers, shellers and buyers seem content to watch and wait until planting is finished and the crop gets up.

Markets are a tad firmer with good demand having been booked into new crop. The thinking is that shellers are comfortable with a bigger crop as an increase in demand from Europe will continue due to an Argentine crop shortfall. Buyers’ ideas remain in the low to mid 50 cents per pound, making it difficult for shellers to want to sell much. Shelled prices for runners for 2022 crop are 61 to 64 cents per pound.

Buyers seem content that there is a big quality crop on the way and are willing to wait at this point. European Union activity for current crop continues to come in as the Argentine crop issues have created a need for U.S. peanuts. There are inquiries for the U.S. new crop from EU buyers, but shellers are reluctant to offer until acres are better understood, and of course the quality of the crop won’t be known until harvest.

Domestic And Export Markets

Raw peanuts in primary products are down 2.5%. Peanut butter is also down 3.6% for the nine months. In-shells are on a roll, up 9.3%, with peanut usage in snacks down 12.5%.

For the past three months, U.S. peanut exports are down 6.14%. Mexico is still the top buyer, up 9%, as Canada drops only 1% compared to the same period last year. China is the third-largest buyer, down 7.73%. Japan jumped up to the number four spot, and the Netherlands is now the fifth-largest export market.

If 96% of sown acreage is harvested and yields improve by 5% to 4,230 pounds per acre, U.S. peanut production is forecast to increase to 6.3 billion pounds or 3,150,000 tons from 5.6 billion in 2022.

After accounting for lower beginning stocks, supply is forecast to reach 8.6 billion pounds, 557 million pounds higher than 2022.

The average price received by farmers is projected slightly down from its expected 2022/23 value of 27 cents per pound, or $540 per ton, to 26.5 cents per pound, or $530 per ton. Moreover, the export program is expected to benefit. The 2023/24 peanut export forecast is 200 million pounds more at 1.3 billion pounds (650,000 tons).

Markets will likely firm up even more after the estimated planted acreage report is released from USDA June 30. Farmers are concerned about the lack of rain early and worry more about the Farm Bill. Peanut leaders have presented new proposals, which all cost money; however, the response is that there is no new money. Some think that peanut producers will be lucky to keep what they have. PG

Farm Bill Update

Last month, representatives of the U.S. Peanut Federation testified at both the U.S. House Agriculture Subcommittee on General Farm Commodities, Risk Management and Credit and the U.S. Senate Agriculture Subcommittee on Commodities, Risk Management and Trade hearings. The purpose of these hearings was to gain producer perspectives on the 2023 Farm Bill and the viability of the farm safety net.

The USPF testimony highlighted peanut priorities for the 2023 Farm Bill, namely an increase in the reference price for the Price Loss Coverage program. Over the past few years, peanut growers have seen a significant increase in the cost of production. According to Stanley Fletcher of Abraham Baldwin Agricultural College and Professor Emeritus at the University of Georgia, the 2021 cost of production was $545.97 per ton, and the 2022 cost of production is approximately $668 per ton.

USPF also testified in support of a voluntary base update that includes growers with and without peanut base acres. While the 2014 Farm Bill allowed for a base update for peanut growers that already had base on their farms, it excluded many young farmers and new production areas.

As we head into the summer, legislators continue their work crafting the 2023 Farm Bill.

Debt Limit Debate May Affect Timeline

Recently, after weeks of negotiations, the U.S. House of Representatives and the U.S. Congress passed H.R. 3746, the bipartisan debt limit deal to avoid a historic default. The deal suspends the nation’s $31.4 trillion borrowing limit until January 2025.

The legislation includes spending caps and limits non-defense discretionary spending to 1% growth in Fiscal Year 2025. This could mean cuts for the agricultural appropriations legislation, which is one of 12 appropriations bills passed yearly. The U.S. House Appropriations Subcommittee on Agriculture, Rural Development, Food and Drug Administration and Related Agencies held a markup of the FY2024 legislation in early May. The markup by the full committee is expected later this summer.

One of the main tenets of the debt limit negotiation was changes to the work requirements for government assistance programs, namely the Supplemental Nutrition Assistance Program and the Temporary Assistance for Needy Families Program. The bill imposes new work requirements on adults ages 50-54 who don’t have children living in their home. The current law only has work requirements on adults 18-49.

When asked about how the debt ceiling deal will impact funding for the Farm Bill, Congressman G.T. Thompson (R-PA), who serves as the chair of the House Agriculture Committee, says the deal will have “no significant impact… The monies overall are capped, but how we invest those and divide those up, Congress has flexibility for that.” However, lawmakers have voiced concerns that lengthy negotiations over the debt limit may cause delays for the 2023 Farm Bill. PG

{kind=link}