Contributing Editor

The peanut market mystery begins again. How many acres will be planted in peanuts this season? Peanut leaders are urging caution. Another 10% increase in acres is likely to oversupply the market for 2025-26. The decision to plant peanuts is an easy one as rotating crops, like cotton and corn, are priced lower than a reasonable cost of production.

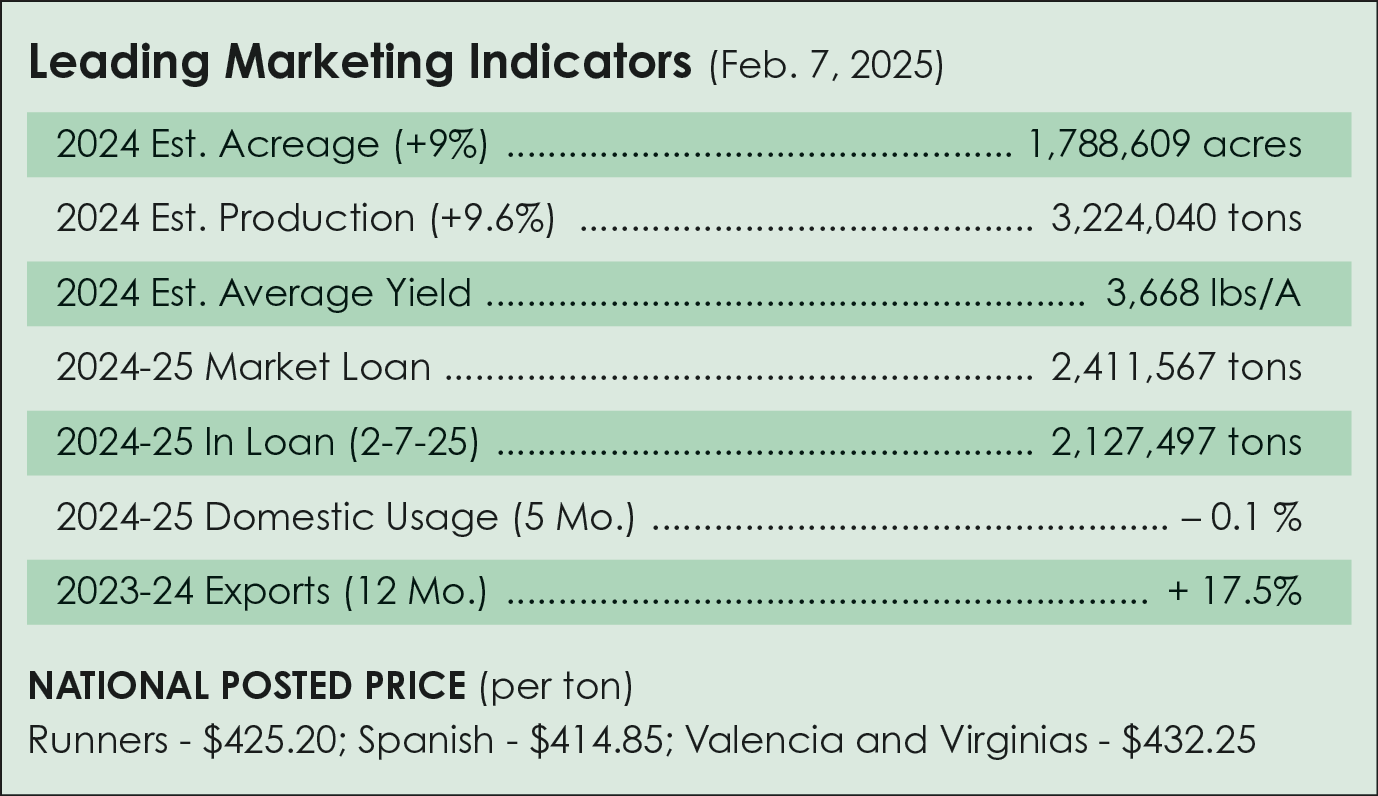

At recent peanut production meetings in Georgia, a survey showed that 45% of farmers present would plant the same peanut acreage as last year. Remember, peanut acreage was up 9% in 2024. The survey showed 18% of the growers planned to increase acreage 10%, and another 14% of farmers said they would increase acreage by 5%.

Good Quality, Reduced Average Yield In 2024

The Federal State Inspection Service report the grading of 3,229,028 tons, 100% of the U.S. Department of Agriculture estimate of 3,224,040 tons. Quality evaluations show that 13,871 tons were graded as Seg. 2s (0.4%) and only 4,950 tons graded as Seg. 3s.

The average yield computed to 3,668 pounds per acre, or 141 pounds per acre fewer than 2023. This was disappointing; however, the reduced production has kept shelled prices firm and farmer prices of peanuts bought from the loan as high as $625 per ton for Southeast runners. At press time, 331,194 tons have been redeemed from the loan leaving about 2,097,187 tons.

Will Anything Wake The Market?

Confusion in Washington, D.C. has farmers worried whether any economic assistance will be deposited into their farm accounts by the USDA Farm Service Agency by planting time. Will banks be willing to take the risk that the money is in the mail?

For peanuts, the estimated economic assistance payment of $76.30 per acre is our part of the $11 billion package. Kernels are being indicated for the remainder of calendar year 2025 around 63 to 64 cents per pound, but buyers don’t seem keen to buy at those levels today. One broker commented that the market was asleep. With shellers working around the clock and supplies in cold storage, there is no rush.

Concerns About Overplanting

With the Farm Bill extended into 2025, the industry still has the $355 per-ton loan available and the reference price of $535 per ton. The average price is predicted to be $536 per ton resulting in no payment to peanut producers from the program.

With cotton at 68 cents per pound and corn at $4.50 per bushel, farmers are strongly talking about increasing peanut acres. Leaders are warning farmers not to overplant.

As this person said it best, “If things go right, we’re going to bust the bank. We’re going to flood the market with peanuts. If we go 850,000 to 900,000 acres in Georgia, and we have 4,100 pounds per acre, we’re going to bust the market. We’re going to go back down to a $400 to $350 contract price, potentially. In previous years that’s what’s happened. You go from $500 down to $375.”

Domestic Demand

The demand for peanuts has improved the past few months, and that is good news for the farmers, provided manufacturers pass along higher-priced orders to shellers. Raw peanuts in primary products is down only slightly in August to December, compared to the same five months of 2023.

Peanut butter usage is a favorable 9.6% increase comparing this past December to December 2023. The peanut butter comeback shows the category about the same as last year. Candy usage is down 5.5% for the five months after a 4.9% decline in December verses the past year. Peanuts in snacks are up 13.8% for the year-long period and is now up 3.8% for the five months.

The USDA summary says overall demand is down slightly from last year, much better than the 4% decline the previous year.

In good news for moving inventory, the government is purchasing and there is a campaign to get peanuts and peanut butter back in the schools. December government purchases were 2.377 million pounds of peanut butter and 51,849 pounds of roasted peanuts. For the five months, government purchases totaled 12 million pounds, an increase of 20%.

Export Markets

Peanut exports continue to increase, in spite of all the tariff talk. With the tariff discussion, markets are either rushing to get product over the border or delaying it until the smoke clears. Funds are being increased for trade promotion programs such as the Foreign Market Development and Market Assistance Program. The top buyers of U.S. peanuts are Mexico, Canada, the Netherlands, China and the United Kingdom. For the past five months, exports are up almost 20%. USAID plants utilizing peanut butter as a therapeutic food are under a stop work order while the Department of Government Efficiency sifts through wasteful spending.

Quiet, But Strong Consumption

There is still much to do in Washington D.C. to write a five-year Farm Bill, but for now, everyone must survive under the one-year extension of the 2018 Farm Bill.

The good news is that the peanut market is strong, even if it is taking a nap. Peanuts and peanut butter have a proven track of positive nutrition. Domestic peanut food use is predicted to increase in 2025. With all the added promotion funds, exports should also increase. The advice from peanut specialists is to take care of tested seed, don’t plant too early, wait for the soil to warm to 65 degrees Fahrenheit for three consecutive days and meet with your local buying point manager to negotiate a profitable contract or option to the loan and gamble to sell your crop from there in 2025.

{kind=link}