Contributing Editor

The peanut market is and has been quiet for months. Manufacturers are not interested in 60 cents-per-pound peanuts and know that the industry has a good quality crop in warehouses, plus a 1-million-ton carryout. There seems to be downward pressure on the shelled market but not enough interest to move the market.

Meanwhile, the peanut producer is faced with increased costs and inflation. Thus far, growers have been unwilling to negotiate and are still studying their options. One official says, “all eyes are on cotton and China.”

There is little discussion about the price of farmer-stock contracts, and time is passing. With the shelled market stalled, manufacturers seek to find prices more along the low 50 cents per pound. Brokers and others describe the market as “dull.” It’s obvious contracting will not begin until shellers get some signals from manufacturers they are willing to buy that level.

Watching Cotton

The highest daily spot price for cotton in 2022 was May 4 at $1.50 per pound. The lowest was Oct. 31 at 72 cents. Cotton acreage and production will decline in 2023 because of lower price expectations compared to competing crops. An optimistic futures price in 2023 is 80 to 85 cents per pound. Conversely, a pessimistic price is 69 to 75 cents per pound. For planning and budget projections, Extension economists suggest a price of 72 to 78 cents.

Supply

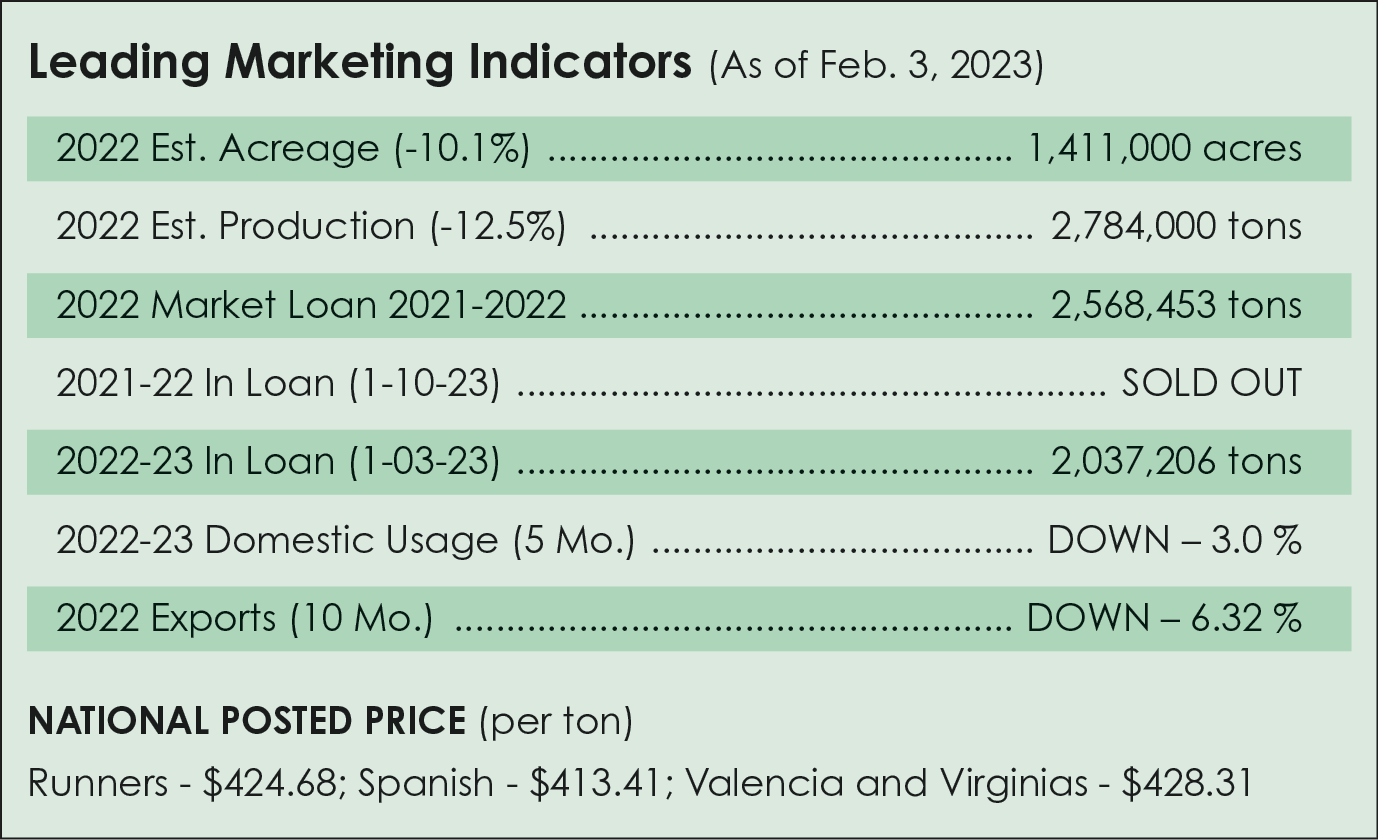

The supply of peanuts was reduced by 2 million pounds last month to 5.57 billion pounds. A yield reduction for Georgia and Alabama and a reduction in harvested area for Texas account for most of the decline. Reduced U.S. peanut production in 2022, resulting from fewer harvested acres and a lower peanut yield of 4,019 pounds per acre, trims the estimated total peanut supply by 203 million pounds, a 2.5% reduction. It still leaves 1.1 million tons as ending stocks and is a market depressor.

The Price Loss Coverage program will not have an impact on the farmer’s plans and could be $5 per ton next October. One sheller recently announced a payout of $22 per ton above contracts and other premiums for seed or irrigation. A new ReGeneration cover crop program may net the famer another $10 per acre. The U.S. Department of Agriculture is initiating new programs for climate-friendly management on the farm.

Exports

U.S. peanut exports are reduced by 100 million pounds to 1.1 billion. Carryout is forecast to remain at 2.18 billion pounds, below the 2021/22 carryout of 2.36 billion pounds.

China has reduced peanut purchases by 39% compared to 2021 (January-October). However, the country has still bought more than 68,000 metric tons of kernels and processed product. Although China is the biggest food importer in the world, they are entering a population crash after 40 years a self-imposed one-child policy. Some reports indicate the population could dwindle from the current 1.4 billion to 1.0 billion by 2050.

Mexico and Canada have purchased more than 56% of the exports with the Netherlands and Japan ranking fourth and fifth, respectively.

Trade Help Needed

Peanut leaders have written the U.S. Undersecretary of Trade and the Chief Ag Negotiator to bring to their attention non-tariff trade barriers of imports from the United States into the European Union, which are being unreasonably targeted for aflatoxin. Fair testing protocols would increase U.S. exports.

The American Peanut Council was approved for $2.4 million for Market Access Program funding projects and $470,000 for Foreign Market Development programs to promote peanuts and peanut products in selected markets in 2023. A group of Congressional leaders have introduced a bill to double the export promotion programs next year.

Argentina has suffered from lack of rain and heat during the early part of the growing season. Estimated planted area is about 375,000 hectares, a 10% to 12% reduction from last year. Rains are needed in February and March. If this happens, Argentina expects a decent crop.

Quiet Markets

Overall, the peanut market summary is the same as last month. The market is quiet as buyers have good coverage and are not wanting to buy into the market at the prices it would take to find a willing seller.

Year To Date Exports

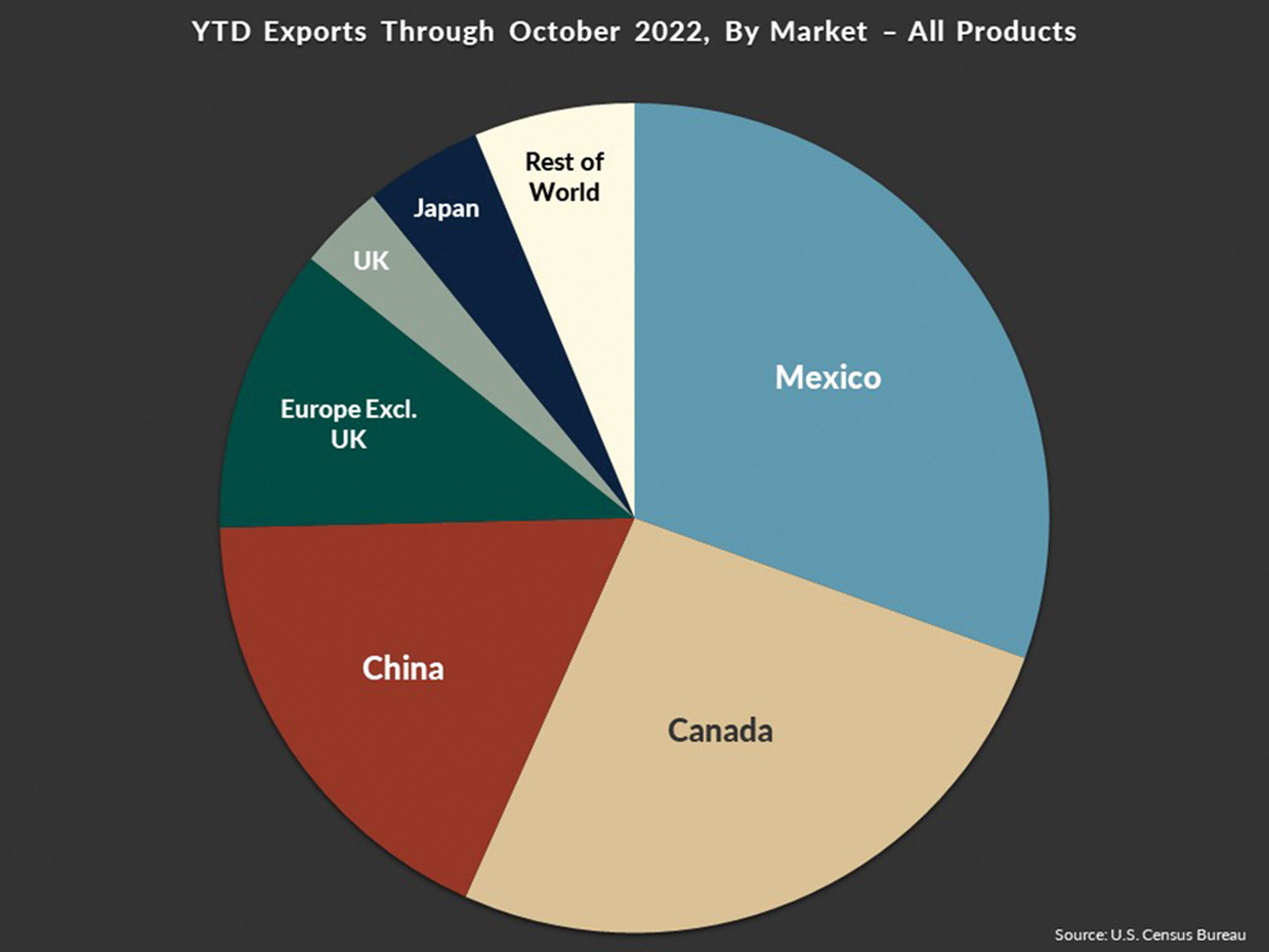

U.S. peanut exports through October increased 2% by value but decreased 6% by volume as compared to the same period in 2021. Total exports reached 404,850 metric tons, valued at $601 million.

Shipments To Japan And Europe Grow, UK Declines

Shipments to Mexico remain strong, increasing 14% by value and 7% by volume to reach $176 million and 123,414 MT. Exports to Canada are also up for the year-to-date, rising 6% by value and 3% by volume to $172 million and 106,061 MT. Exports to China decreased 30% by value to $69 million and 38% by volume to 72,668 MT. Shipments to Europe, excluding the United Kingdom, increased 12% by value and 10% by volume to reach $64 million and 44,992 MT, while shipments to the UK decreased 3% by value to $21 million and 13% by volume to 13,270 MT. Exports to Japan increased 18% by value and 28% by volume to reach $33 million and 18,616 MT, respectively. Finally, exports to the rest of the world rose 4% by value to $67 million but decreased 1% by volume to 25,379 MT.

By Product Type: PB And Processed Peanuts On Upward Trend

The U.S. exported 154,274 MT of raw kernels valued at $204 million through October, down 27% by value and 34% by volume as compared to the previous year. Shipments of inshell peanuts (including farmer stock) totaled $120 million and 111,169 MT, up 3% by value but down 11% by volume year-over-year. Blanched peanut exports increased 213% by value and 354% by volume to reach $82 million and 64,636 MT. Peanut butter shipments have also increased, rising 7% by value and 5% by volume to $119 million and 37,029 MT. Finally, exports of processed peanuts totaled $55 million and 21,318 MT, up 32% by value and 37% by volume.

For more information on year-to-date U.S. peanut exports, visit PeanutsUSA.com.

{kind=link}