Contributing Editor

The 2023 peanut season had many unusual challenges that tested producer’s management skills. In the Southeast and Virginia-Carolina regions, the season started with some dry, some wet, but overall cool conditions. The slow start had seed officials and others reporting that seed vigor was being tested in the cold soils, which delayed emergence up to two weeks.

In Georgia, farmers were reporting problems with stands, poor germination and checking with crop insurance about replanting.

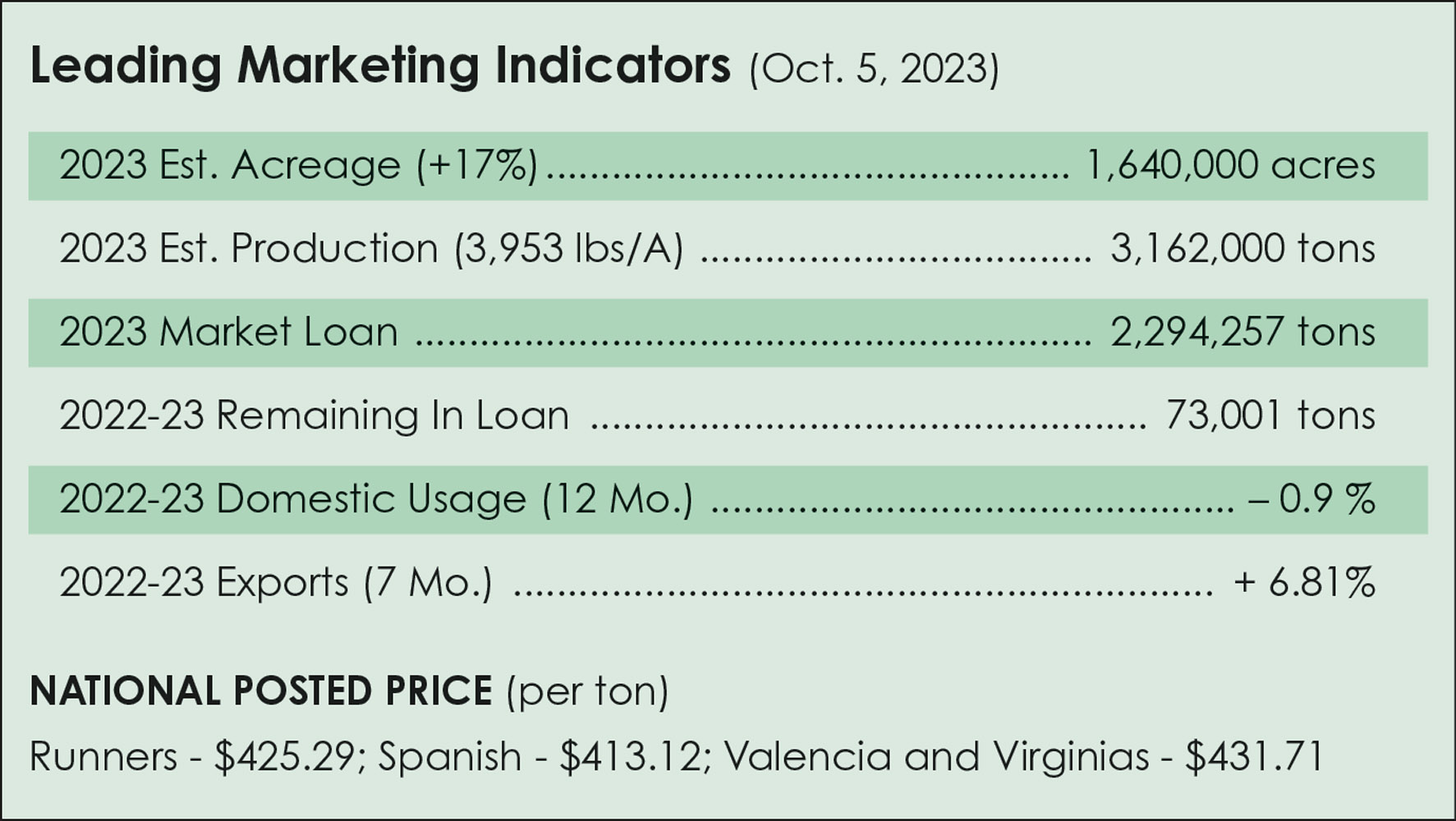

Contract offers were not a bright point, either, because of increased costs of production and inflation. Everything the farmer buys has increased. Even so, industry analysts predicted an increase in peanut acreage if cotton futures stayed the same. In March, the U.S. Department of Agriculture predicted peanut acreage to increase 7% with Georgia up 8%. Each state’s peanut specialist had already sounded the alarm predicting peanut acreage to increase 9.6%. By September, peanut acreage as USDA certified or reported was up 14%.

No Competition For Land

The competition for tillable land from cotton, corn or soybeans never materialized. Cotton stayed near 80 cents per pound and was up 10% in acres. Corn acres were up 10% as well.

Producers argued that last year’s 2.7-million-ton crop, on the smaller size, and the 18%-plus increase in costs of production merited a higher offer for 2023 contracts. An ag economist found the 2022 cost of production was approximately $668 per ton. Still, shellers started their offering at $500 to $525 per ton for runner-type peanuts, $525 per ton on high-oleic varieties and $550 to $575 per ton on Virginia type.

Some shellers offered a sheller pool with a $500 per-ton floor hoping prices would increase later this season. Prices were higher for Southwest varieties because of the cost of production for irrigated peanuts. Farmers who had joined a local co-op were faced with a decision to deliver co-op stock tonnage or revert to selling to a local sheller for offers of $600 or more. Tempting, but illegal.

On The Positive Side

Some good news in the market is that before peanuts were harvested, shellers offered a $25 per-ton bonus in response to buyers wanting to get contracts signed for delivery. Another news flash is that the 2022-2023 market loan is almost paid back to the government. That crop had more than 2.29 million tons of peanuts in the loan with a $355 per-ton guarantee and the government has been repaid, down to 15,200 tons at press time. That makes two years in a row with no forfeitures to the government. The peanut program works.

Part Of The Program Not Working

As the crop has been behind much of the season and harvest stretched later into the fall, questions about the crop have surfaced, stalling the peanut market. However, it does remain firm as a problematic growing season with certain areas experiencing significant drought has prompted questions about yields and, unfortunately, quality.

Shellers are taking a wait-and-see attitude to selling until the crop is dug and shelling begins in earnest. Shelled prices for runners for the 2023 crop are 64, 63 and 62 cents per pound (LMS). Prices usually decline at harvest with the new supply. USDA estimates 3.1 million tons produced from 1.64 million acres at an average of 3,943 pounds per acre.

The peanut program has one segment that is no longer working. The Price Loss Coverage/Agriculture Risk Coverage program has not been updated, and now the average price paid to farmers is lower than the reference price. The effective reference price for peanut is $535 per ton. The higher of the loan rate at $355 per ton or market price average at $540 per ton is deducted from the Reference Price $535 per ton. That’s a negative, so it means the PLC payment for 2022-2023 is $0.

Domestic Market

Raw peanuts in primary products is down almost 1% for the year. Peanut butter continues to set new records, up 5% for the year and up 3% compared with July 2022. In-shells continue strong, up 14.6% for the year. Peanuts in candy declined almost 10% for the year with raw peanuts used in snacks down 6.1%. Raw peanuts used for government nutrition programs showed down 51%.

But there is good news, 70% of all consumers have a snack every day. They average three snack times per day, and 66% of consumers have an indulgent snack at least one time per week.

The Peanut Institute has announced that peanuts and peanut butter can produce compounds in the gut that help improve memory and reduce stress response, including anxiety and depression, in healthy young adults. Domestic markets are forecast for a 3.7% increase in 2024.

Export Market

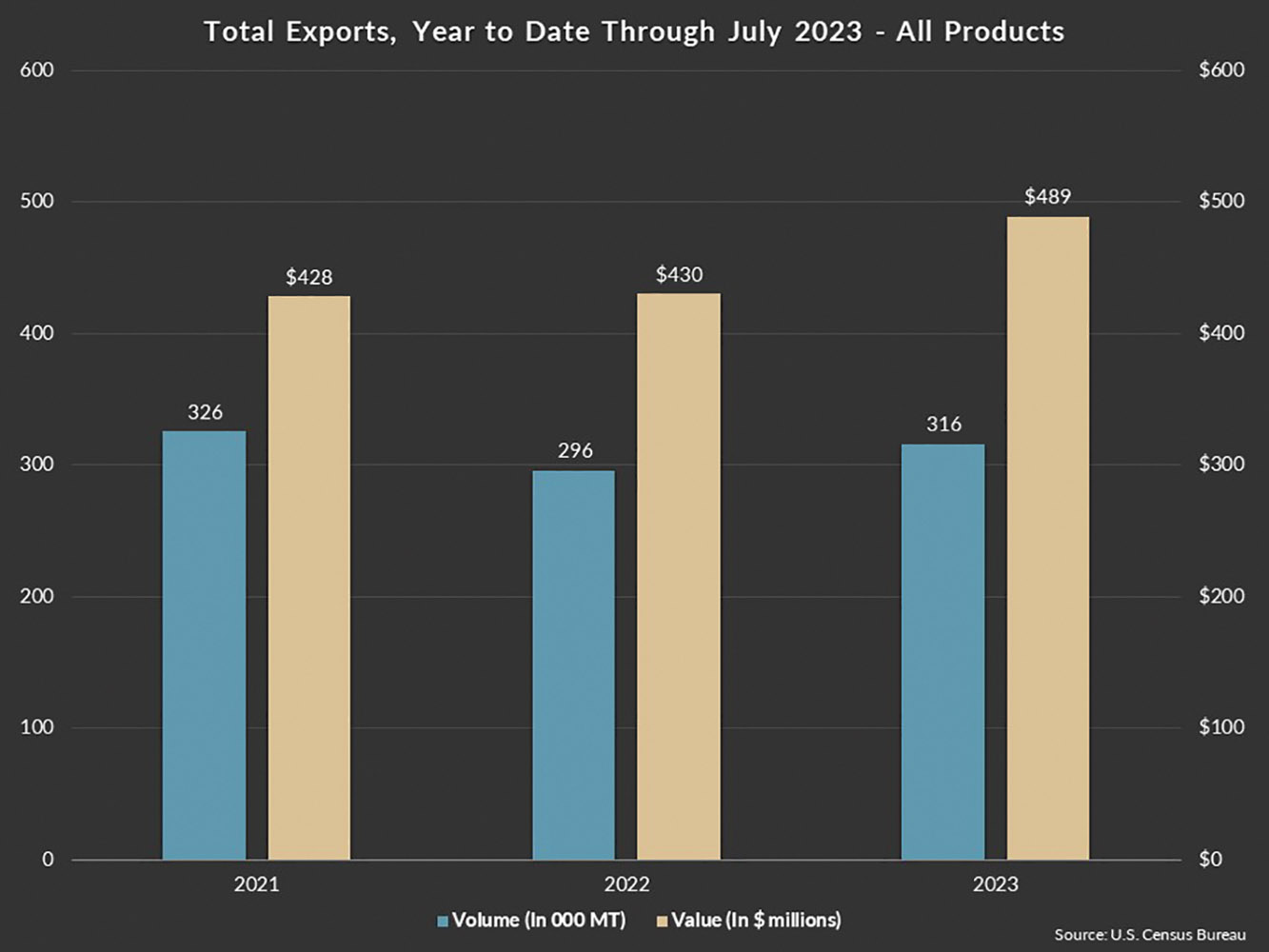

U.S. peanut exports for the year through June increased 7% by volume and 14% as compared to the same period in 2022. Total exports reached 316,283 metric tons, valued at $489 million.

Mexico remains the top international market for U.S. peanuts, with shipments increasing 0.4% by volume to 88,134 metric tons. China surpassed Canada as the second largest importer of U.S. peanuts for the year. With a higher supply, U.S. peanut exports increased this month to 675,000 tons, up 12.9%.

The peanut industry is in a good position. Expansions are being reported in all segments. This plant-based protein is being recognized around the world. The future is bright. The nutrition can save lives and increase lifespan, and we’ve even learned it improves memory. Like President Carter said as he celebrated his 99th birthday, “If you want to live a long and healthy life like me, eat more peanuts!”

China Surpasses Canada As Second Largest Export Destination

Shipments to the Chinese market increased 25% by volume and 37% by value to reach 74,378 metric tons and $74 million, as the country surpassed Canada for the position as the second largest importer of U.S. peanuts.

Exports to Canada, the third largest destination, totaled 71,617 metric tons, valued at $122 million, down 3% by volume and up 2.5% by value as compared to 2022.

Shipments to Europe, excluding the United Kingdom, increased 34% by volume and 57% by value to reach 43,353 metric tons valued at $71 million. At the same time, exports to the UK fell 37% by volume and 29% by value to reach 6,090 metric tons and $11 million.

Exports to Japan have decreased 19% by volume and 17% by value to reach 12,068 metric tons and $21 million. Finally, shipments to the rest of the world grew 12% by volume and 36% by value to reach 20,643 MT and $62 million.

In-shell peanut exports increased 49% by volume to 120,225 metric tons and 71% by value to $142 million through July. Exports of raw peanut kernels fell 31% by volume to 82,578 metric tons and declined 27% by value to reach $114 million. During the same period, shipments of blanched peanuts increased 34% by volume and 46% by value to reach 61,072 metric tons and $84 million according to official statistics. Year-to-date peanut butter shipments increased 12% by volume and 16% by value to reach 28,659 metric tons and $95 million. Finally, exports of processed peanuts increased 10% by volume and 14% by value to 15,684 metric tons and $42 million.

{kind=link}