Contributing Editor

The peanut market is very quiet. Shellers have enough inventory to sell for the year but are remaining firm, which is garnering little interest, especially for the 2022 crop. Markets for raw product remain in the mid-50s. The standstill in contracting the 2022 crop may have something to do with farmers’ bullishness on cotton and corn, which at these levels will compete with peanuts for acreage. A farmer-stock price of $475 per ton is not too interesting to farmers.

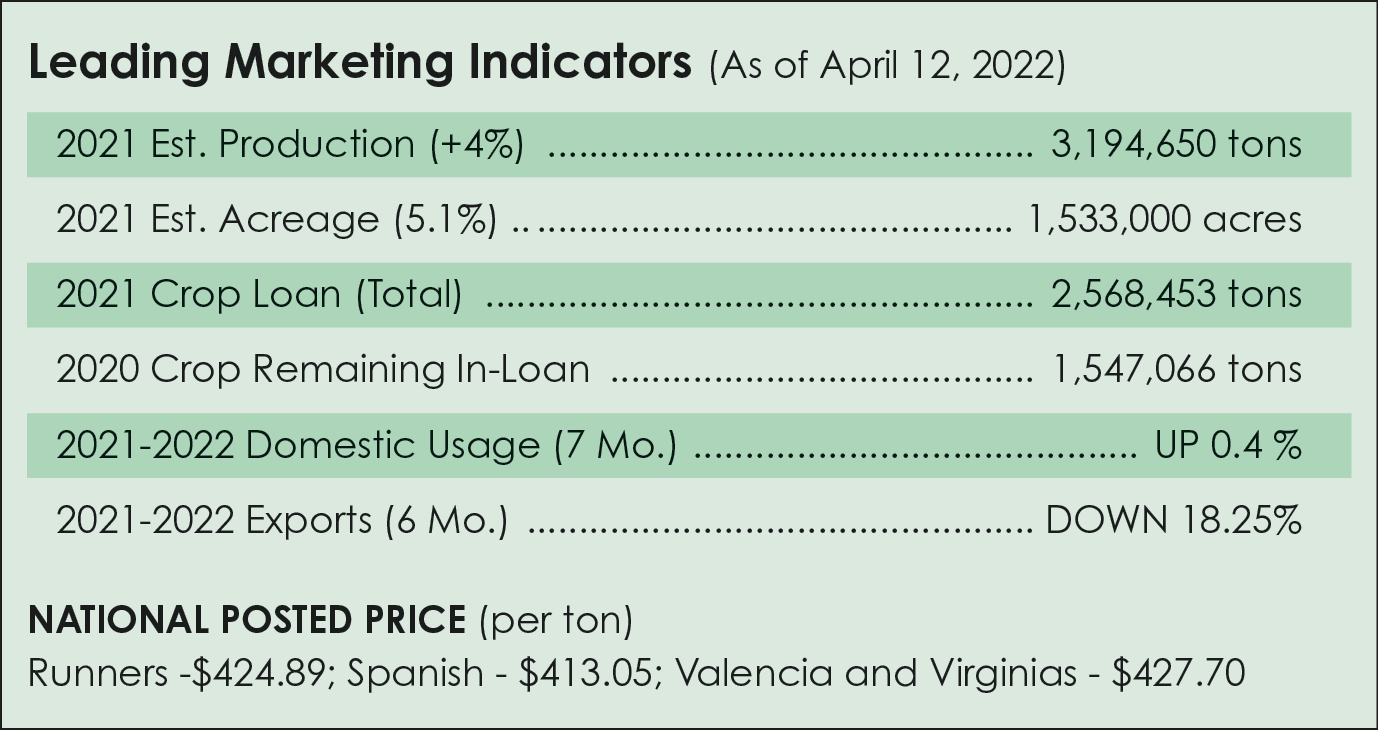

Contracts have ranged from $500 per ton for limited tonnage on runners to $600 per ton for Virginias and even higher for Valencia and Spanish in the Southwest.

Both sides are content to wait, and buyers are watching the markets as they have good coverage for 2022 in the books. Buyers wanting to book peanuts for the 2023 calendar year did so earlier this year when offers were available, but most thought that was too risky.

Markets At A Standstill

Uncertainty has been the buzz word these past few months. Uncertainty over new crop peanut acres has been influenced by the corn market’s slow and steady climb. Putting downward pressure on that market were increased input costs from fertilizer. Peanuts benefit from not needing direct fertilizer. More uncertainty comes from escalating cotton and soybean futures along with soaring diesel costs.

Russia’s invasion of Ukraine has only fueled rising commodity markets and input costs to growers. It has also led to rising sunflower oil prices and uncertainty over South American peanut exports to the two warring countries.

This uncertainty has fed an unwillingness from growers to contract farmer stock and a lack of buying interest at levels that support what most think it would take to buy peanuts from a grower. In this market, shellers are not able to or willing to do much marketing on 2023 peanuts and, to some extent, on the current crop.

Competition For Acres Abroad

The next market factors to watch are plantings beginning in the second half of April and weather through the summer as a La Niña pattern is predicted to reach the East Coast by the end of June. The country is in drought from California through Texas to date. With the Ukraine/Russia war and crop plantings of wheat and sunflowers at risk there, the price of various food commodities has skyrocketed. Demand for vegetable oils worldwide and the crimp in supply for sunflower and soy oils, has pushed peanut and other oils prices higher with no relief in sight.

Both Argentina and Brazil are harvesting their peanut crops, and Argentina experienced several nights of frost in early April. Going forward, with much higher land rents and competing crops due to vegetable oil demand, both countries will be hard pressed to plant similar peanut acreage for the next crop.

Toss in the normal uncertainty in the peanut market regarding future interest from China in U.S. peanuts, a dash of doubt over where Argentina and Brazil may go with their crop if they can’t export to Russia and/or the Ukraine and stir in the unknowns about weather and crop quality. With all the unknowns, market uncertainty increases.

Acreage Estimate

With the 2021 crop being one of, if not the best, in terms of quality, it is easy to see why sellers would want to hold on to unsold goods until new crop gets planted and its development is better known.

It is difficult to get offers on new crop for 2023, particularly from the Virginia-Carolinas and the Southwest, but Southeast offers are not easy to come by either. Given the uncertainty on what shellers may have to pay to contract 2022 farmer stock and the shelled-goods market not aligning with prices that support levels it would take to contract, we are in a wait and see mode.

The U.S. Department of Agriculture National Agriculture Statistics Service prospective planting report shows a decline of 0.9% for the 2022 crop. Growers intend to plant 1.57 million acres in 2022, down 1% from 2021. In Georgia, the largest peanut producing state, expected planted area is down 3% from 2021. If this acreage amount is multiplied by the average of 4,000 pounds per acre, and a 2.5% decline for planted area versus harvested, the United States will end up with a projected production of 3.063 million pounds. This is plenty of peanuts for the amount of demand unless China returns to the market.

Eyeing Changes In November

Another part of the puzzle is the price-loss coverage payment in October. As the average price of peanuts increases, that means less of a PLC payment. In March, USDA estimated a $51 payment, which would apply to 85% of the farm peanut base. That is not much, but every little bit helps.

The U.S. Peanut Federation continues to meet with Farm Bill planners in hopes to continue the peanut program. Leaders understand that the present slate of Washington leaders could all change after November elections and Farm Bill negotiations would have to be repeated.

With all the uncertainty, including a possible food shortage, it is a good time to buy a few extra jars of peanut butter. PG

{kind=link}