Contributing Editor

Peanut producers roll into 2024 with lower commodity prices and higher inflation. The U.S. Department of Agriculture predicts that farm income will drop 25% from last year, news that took center stage at their recent Agricultural Outlook Forum. The government agency forecasted season-average corn and soybean prices of $4.40 and $11.20 per bushel, respectively.

Cotton producers intend to plant 9.8 million cotton acres this spring, down 3.7% from 2023, according to the National Cotton Council. The NCC says fewer cotton acres for 2024 are a result of weak demand and higher input costs putting pressure on profitability.

For peanuts, a survey of growers found that peanut acres will increase 5.4% to 1,731,000 acres. Georgia peanut producers are expected to plant 820,000 acres, up from 770,000 acres this past year, for a 6.5% increase. Other growing areas, both new and old, all show increases in peanut acreage: Arkansas +17.6%, Alabama +6.9%, Florida +6.5% and Mississippi +11%. The USDA National Agricultural Statistics Service’s Prospective Plantings Report will be released March 28.

Final 2023 Numbers

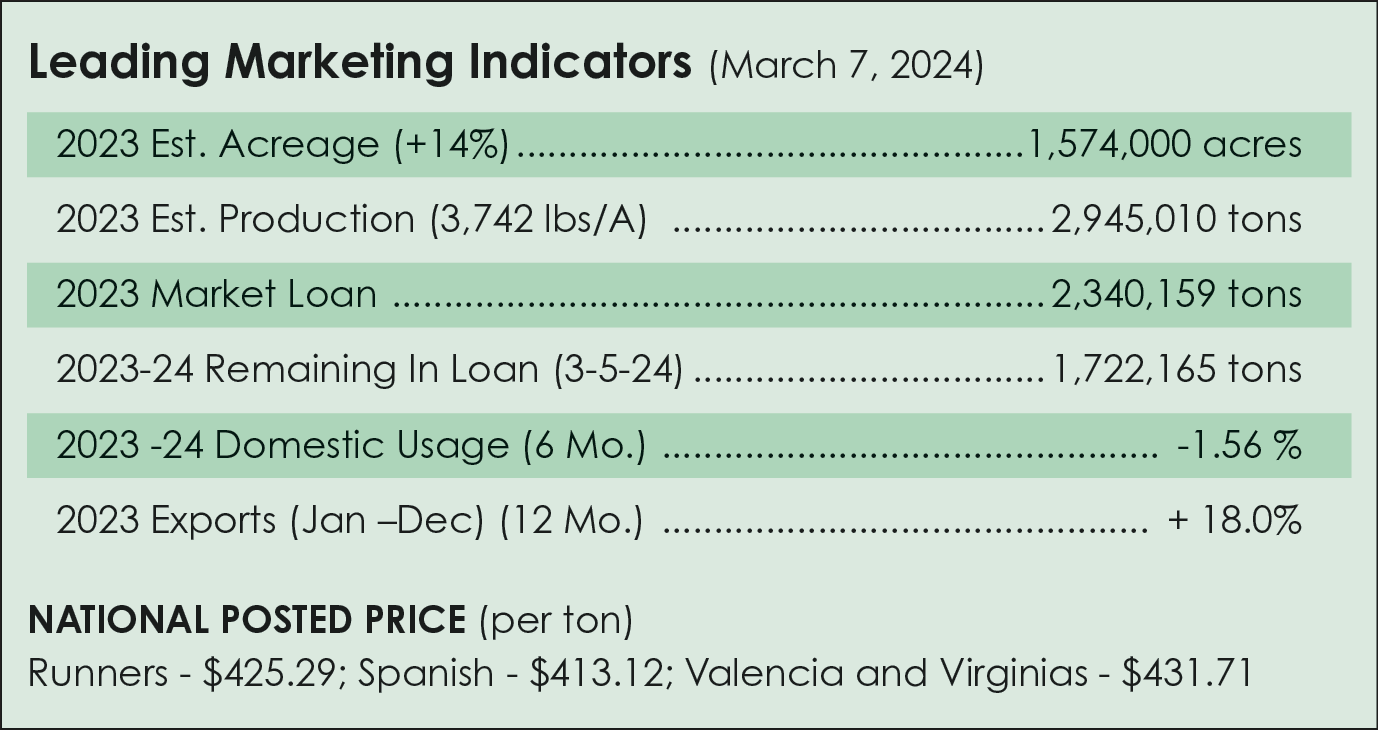

Looking back, the peanut market remained strong in 2023, but higher input costs persisted as a major challenge. Contracts were largely in the range of $500 to $550 for runner peanuts for a second consecutive year. In the 2023–2024 marketing year, there was a 14% increase in planted peanut acres nationwide, to 1.65 million acres.

U.S. peanut yields were projected to average 3,742 pounds per acre, well below the 10-year average of 3,942 pounds per acre. The national peanut yield would be the lowest since 2016. In Georgia, peanut yields are expected to be down 3% from the previous year at 4,100 pounds per acre, also the lowest since 2016. Overall, U.S. peanut production increased by 7% to 2.9 million tons.

USDA NASS says the price of peanuts averaged $0.270 per pound ($540 ton) last season, 0.7% higher than 2022. The value of the 2023 peanut crop at farm level is $1.6 billion, a 7.5% increase from 2022. The average price was higher than the reference price of $535 per ton eliminating any Price Loss Coverage program payment.

How Is 2024 Shaping Up?

In the Southeast, buying points report shellers are offering a contract for runner-type peanuts at $550 per ton for high-oleic varieties and $525 per ton for regular-oleic peanuts. Tonnage is limited for each buying point. Additional bonuses, such as $25 per ton for irrigation, are being offered in some areas. Those shellers who are not buying high-oleic type cultivars are matching the $525 per ton for regular-oleic varieties.

In the Virginia-Carolina region, buying points report contracts are being offered at $525 per ton for runner-type peanuts, $550 per ton for high-oleic peanuts and $545 per ton for Virginia-type varieties.

The near-term market remains very firm. It’s difficult to get offers, and prices remain in high 60 cents per pound to 70s depending on the grade and specifications. New crop buyers are convinced there will be more peanuts planted in ’24, so they are looking for offers in the mid-50 cents per pound.

Domestic Markets

What about the U.S. market? Raw-shelled peanut usage is down 1.56% for the six-month period of August through January in primary products. Peanut butter shows an increase during the same period of 1%. Peanut candy took a fall in January; however, usage is down only 1.2% for the six months. Snacks were down 11% for the year. There were no deliveries under the Government Domestic Feeding and Child Nutrition Programs for January. Deliveries for the year totaled 10.3 million pounds, 40% more than the previous year.

Export Demand

The American Peanut Council reports that total U.S. peanut exports for 2023 reached a record-high value of $889.5 million, a 24% increase from the previous year. U.S. peanut export volume for 2023 reached 562,927 metric tons, up 18% from 2022.

A sharp increase in demand from Europe is the main factor behind the increase. The APC says exports to Europe, not including the United Kingdom, rose 148% by value and 117% by volume to reach $182 million and 110,756 metric tons. At the same time, Europe’s overall share of exports by value doubled year-over-year, rising from 10% in 2022 to nearly 21% in 2023, surpassing China to become the peanut industry’s third-largest export market.

Mexico remained the top export destination for U.S. peanuts in 2023 with total shipments reaching a new high of $230 million and 155,532 metric tons. This represents the third consecutive year that shipments to Mexico achieved a new record. Total exports to Mexico increased 8% by value and 4% by volume as compared to the previous year.

Canada retained the title as the U.S. peanut industry’s second-largest export market with 2023 shipments totaling $218 million and 128,319 metric tons, up 5% by value but down 0.2% by volume. Canadians consume most of the product in peanut butter.

Peanut exports to China increased 24% by value and 21% by volume to reach $98.5 million and 100,843 metric tons. China continues to be a big market for U.S. inshell peanuts in particular, which are typically crushed for oil but can also be shelled and sold to snack and confectionary manufacturers.

Still Waiting On A Farm Bill

What about the peanut program and Farm Bill? With no PLC payment, the peanut program is of less value to the farmer. The $355 per-ton loan value allows some financial guarantee along with storage and handling assistance. Producers are facing opposition to increasing the reference price by some legislators. The U.S. Peanut Federation continues to work toward this effort in Washington D.C., while also trying to keep peanuts in their section of the Farm Bill.

Watch for market offers. International buyers and domestic manufacturers are willing to pay a reasonable price that would hopefully be a profitable enough price to the farmer. They want and need your quality peanuts. Check with your buying point and sheller and stay abreast of industry issues in the works to keep you profitable and sustainable.

{kind=link}