Contributing Editor

Peanut producers look back at the 2022 crop questioning what happened. King cotton was competing for land with unbelievable prices at $1.30 per pound. With inflation rampant and cost of production steadily increasing, the grower worked to reduce inputs when possible.

The weather joined in the battle with a five- to six-week drought across most of the Southeast peanut belt just a most plants were starting to peg. The Southwest production area had little rain all season. Farmers and researchers kept seeing outbreaks of Tomato Spotted Wilt Virus, but it was too late to take any preventive measures.

War in Ukraine was said to be the cause that sent fertilizer prices soaring. Gas and diesel fuel kept getting higher. So many unknowns made a grower wonder about pricing and/or contracting. Was the crop estimate accurate? Was acreage really down 10%, and would prices go higher if the crop was short? The peanut picture is slowly coming into focus.

Production

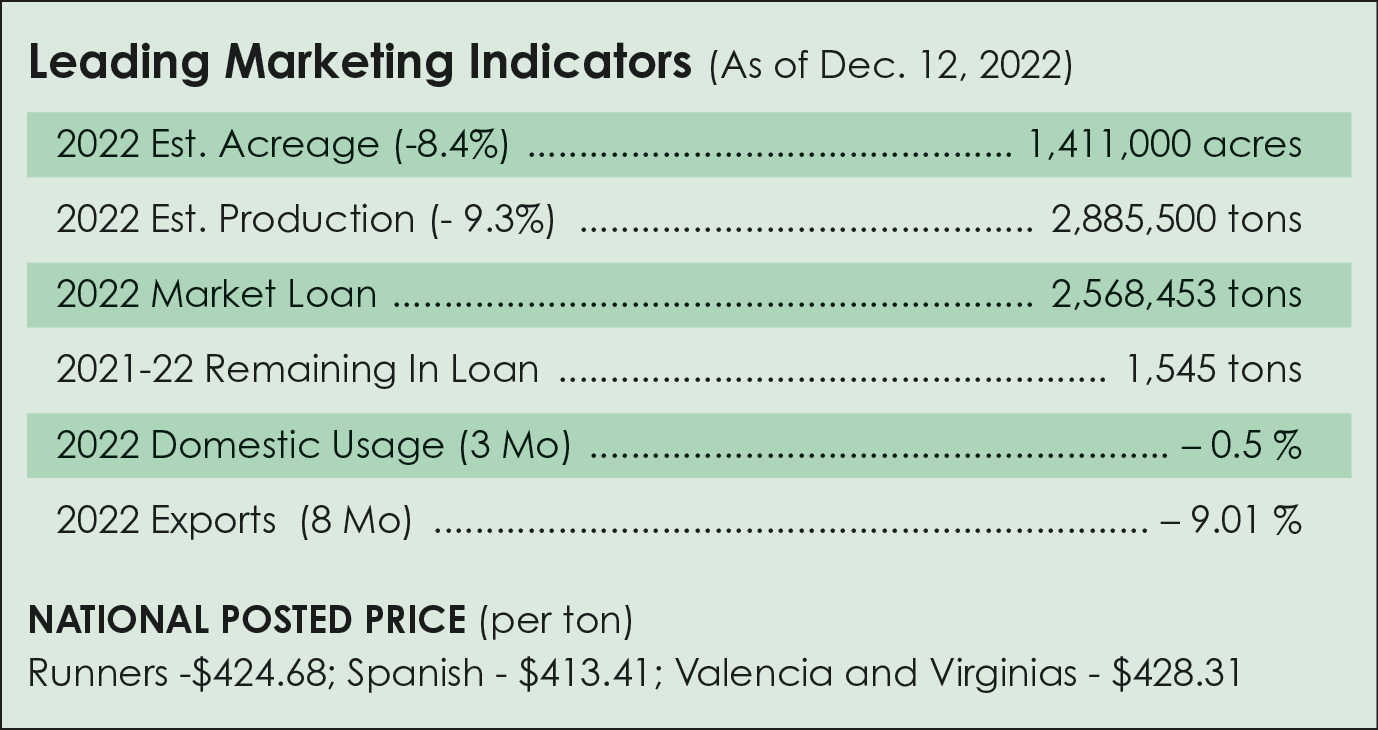

The 2022 peanut yield forecast was reduced to 4,090 pounds per acre from 4,145. Farmers reported peanut acreage at 1.4 million acres, down 8.4%. Total production was estimated at 2.88 million tons, down 9.3% from last year. The Federal State Inspection Service had graded 2.7 million tons by Dec. 9. Only 9%, or 242,531 tons, were for commercial sale at the time, and the remaining 91% was placed in the loan program for $375 per ton.

The quality of the 2022 crop was exceptional. Only .0014% of the crop went Seg. 2 or Seg. 3.

Contracts

Peanut markets remain relatively quiet at the farm level except for uncontracted peanuts. Farmers who did not sign earlier contracts at $500 to $525 per ton were chasing rumors of $625 to $650 per-ton peanuts with shellers offering mostly $600 per ton maximum. Co-ops offered less-promising dividends. The problem is that the peanuts are in the sheller’s warehouse, and that is the only price option available for uncontracted peanuts.

Price loss coverage payments are made when the market year average, which is based on the average prices paid to farmers from August 2021 to July 2022, is below the reference price. The peanut market year average last year was $.2430 per pound, or $486 per ton.

The effective reference price for peanut is $.2675 per pound, or $535 per ton. The higher of the loan rate ($.1775 per pound, or $355 per ton) or market price average ($486 per ton) is deducted from the reference price ($535 per ton). This equals a PLC payment of $49 per ton.

This payment can only be applied to 85% of the peanut farm base. Farm Service Agency payments were verified and paid to the farmer in October 2022.

The U.S. Department of Agriculture has issued a projected market year average price based on world agricultural supply and demand estimates. The projected market year average price for peanuts in August 2022 is $.2650 per pound, or $530 per ton. Deducting $530 from reference price of $535 per ton means the PLC payment next October would be $5 per ton.

The good news from USDA and the Commodity Credit Corporation is that only 1,545 tons remained in the loan in mid-December and are likely sold by now. To begin the market year with 2.56 million tons and have the loan program repaid and peanuts moved into the market is a credit to the USDA team and the buyers, and it merits a renewal in the Farm Bill.

Domestic Market

Good news on domestic markets as October shows a 3% increase for shelled edible peanuts, and peanut butter buys are up 6.7%. For the three-month period, usage is down 0.5% for shelled edible peanuts, while peanut butter shows a 2.7% increase for the same period. Peanut candy and peanut snacks posted slight declines but are still a strong market volume.

Export Market

Mexico and Canada continue as the best export markets for U.S. peanuts. Mexico is up 13%, and Canada is up 3%. Although China is down 45%, it is still a major market. The Netherlands and Japan continue to grow, although total volume is down 9% for the eight-month period.

Heading into the holidays, demand for peanuts is very muted. Normally this time of year, the market for the 2023 crop is pretty active, but this year is different. Because of the higher prices for the 2022 crop, the chances of early contracting for the 2023 crop are slim.

2023 Market

Shellers aren’t going to contract and go long on the 2023 crop if buyers will not support the shelled prices, and farmers aren’t likely to accept $450 to $500 for farmer-stock basis. The market is watching two drivers of future prices.

Because of strict COVID-19 protocols in China, which may only loosen slightly this year, don’t expect the Chinese to show interest in U.S. farmer stock until Fall 2023 at the earliest.

A second market driver is the price of cotton. Priced in the 70s, cotton is not competition for peanut acres, currently, so the assumption is we will have more peanut acres planted. Thus, the price of shelled peanuts should begin to decrease in the spring if a larger crop is planted. Prices remain for grades in the mid-to-low 60s for today and is not likely to decline soon.

In summary, the market is super quiet as buyers have good coverage and are not wanting into the market at the prices it would take to find a willing seller. Supply is adequate for now, but if we need an increase in acreage for 2023, are manufacturers willing to pay? PG

{kind=link}