Contributing Editor

The peanut market is quiet and has been all winter. Trade considers this market very firm, especially for any needed shelled mediums and jumbo runners. There does seem to be a shortage of jumbo runners as the outturn this past year was lower, and there is a squeeze based on this reduced supply. Quality may be better than expected, though, which is a good thing.

Blanching capacity remains strained with a real scarcity of blanched material spot loads. Availability of some specifications should improve by April and moving forward, but relief in the shelled-market price is not likely until this year’s crop is underway.

The current crop market is more like 69 cents per pound for splits and 70 cents per pound for whole kernels if you can get an offer. The market for new crop is around 57 to 58 cents per pound for splits and 59 to 60 cents per pound for whole kernels. Peanut analysts will often say there is no direct relationship between the prices offered to farmers and shelled-market prices.

Planting Without Contracts

Domestically, there are still some buyers who are waiting for falling prices that have not materialized. Some buyers purchase monthly to cover their positions. Many producers placed peanuts in the loan, also hoping for higher prices before time runs out.

Farmers are quick to point out that as prices go up in the market, they should also be paid a higher price. After all, production costs just keep rising. The current price of 70 cents per pound is the likely cause for some shellers to offer $650 to $675 per ton for uncontracted peanuts as manufacturers become concerned about the supply.

There are new crop rumblings from both sides, farmers and shellers, but farmers are not prepared to take $550 per farmer-stock ton after getting as much as $650 last year. Many farmers will wait and plant without a contract this year since delays in signing have been beneficial the past two years. Cooperative farmers are required to deliver to stock tonnage levels, and final dividend payments are received later in the season.

Domestic Production

Producers are faced with low commodity prices all around. With cotton and corn prices at a low levels continuously, more peanuts are likely to be planted for 2024. Who knows what chaos the recent Dicamba ruling out of Arizona will do to the cotton market.

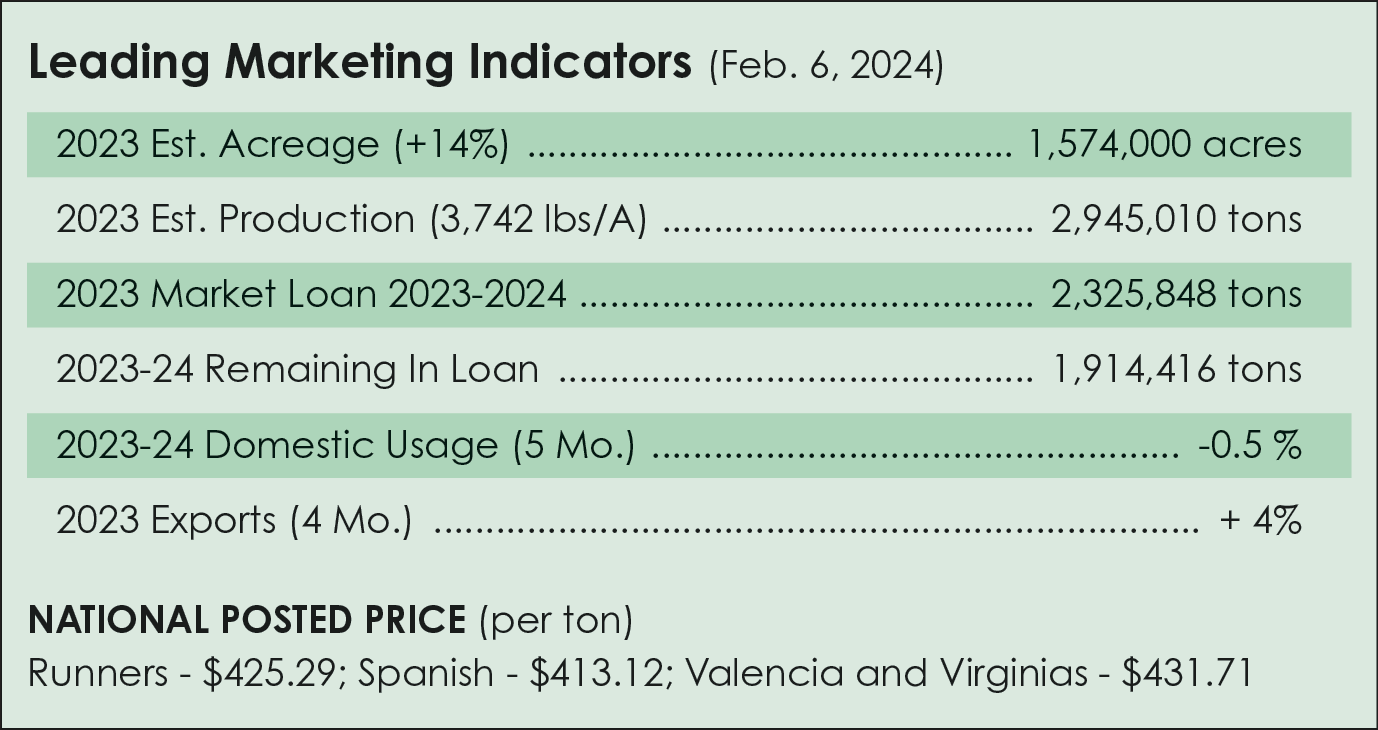

The U.S. Department of Agriculture reduced production of this past year’s crop by 93 million pounds to 5.9 billion pounds or 2.9 million tons on reduced harvested acreage. Average yields are currently figured at 3,742 pounds per acre, down 7% from last year. Harvested acreage is reduced largely in Texas because drought resulted in higher crop abandonment rates, but acreage overall increased by 14%.

Export Markets

Peanut exports are forecast up 25 million pounds to 1.3 billion pounds as the United States has increased shipments to Mexico, Canada and the Netherlands. From August through November 2023, the United States exported 497 million pounds of peanuts, up 4% from last year.

Peanut crush from August through November 2023 was 226 million pounds, down 23% from the same period last year. With strong exports and lower domestic production, crush is reduced by 25 million pounds to 750 million pounds. Ending stocks are lower by 0.1 billion pounds to 1.9 billion pounds, the lowest since marketing year 2016/17.

As of January, peanut stocks in commercial storage totaled 4.81 billion pounds equivalent farmer stock, compared to 5.05 billion pounds last year, down 6.2%. USDA reported raw-shelled peanut usage down 0.5% for the five-month period in primary products with peanut butter showing an increase during the period of 0.6%. Peanuts in candy made a recovery, up 4.5% over the same five months through December.

Another Farm Bill Extension?

Shellers are offering incentives to encourage farmers to continue peanut crop rotation. One sheller had a payout of $8 per ton, to be paid on eligible tons this year. Funds were released Jan. 1, 2024. The ADM re:generations™ program has delivered an incremental $30 per ton above market-based contracts back to growers.

Don’t forget the price loss coverage program. The average price paid to farmers in December 2023 was $498 per ton. That is lower than the $535 per-ton reference price, and a 12-month average could trigger a payment next October.

Market trends are positive for peanuts. Domestic demand is steady, export markets are increasing and new nutrition studies prove that peanuts are positively associated with improved thinking, reasoning and memory.

Finally, don’t be surprised if the Farm Bill is extended another year.

Farming To Breakeven In 2024

With an entire month of the new year behind us, meeting season is in full swing. This season is a time when many agricultural economists get the opportunity to provide market outlooks for the upcoming year for the commodities producers grow and the inputs used to grow them. Last week, a producer approached me at the end of a meeting and commented that it appears like they may be, “farming to breakeven in 2024.” That comment gave me an idea for a teachable moment on planting decisions and variable costs.

Producers’ decisions on what they plant are based on a variety of factors including crop rotation, yield history, expected market prices, estimated input costs, weather expectations and availability of credit. Planting decisions are a short-run decision (i.e. decisions that impact the current crop year). On the other hand, long-term decisions impact multiple years (i.e. investing in irrigation equipment). When making decisions in the short run, it is important to cover total variable costs. Total variable costs for a crop are what it costs to plant, grow, harvest and market the crop. Producers should calculate their cost of production to help them calculate the market prices and/or yields they need to achieve to cover their variable costs.

Given a producer is able to estimate their cost of production, there are two ways to calculate breakeven. The first is through calculating the price needed to breakeven. Breakeven price can be calculated through the following formula: Breakeven price per unit of yield = Total variable cost per acre/expected yield per acre.

The second way to calculate breakeven is through yield. Breakeven yield can be calculated through the following formula: Breakeven yield per acre = Total variable cost per acre/expected price per unit of yield.

Individual producers should keep in mind that their variable costs and cash land rents may differ. Producers are encouraged to utilize tools like enterprise budgets to help estimate their cost of production, breakeven prices and breakeven yields. Understanding breakeven prices and yields can aid producers in management and marketing for the upcoming production season.

{kind=link}