Contributing Editor

The peanut market remains quiet from both the buyer and seller side. There is availability for current crop in the mid-50 cents per pound, but no sellers for new crop. Buyers are aware that carryforward numbers are high, and there is no urgency to book any additional peanuts.

Shellers cannot contract peanuts from farmers for the new crop, and they don’t want to sell to manufacturers. Shellers are off the market as farmers are unwilling to contract at the offer of $500 per ton for runner peanuts and Virginias at $600 per ton. There is not much downside in the market with higher production costs, but any dry weather or other adverse growing conditions, and we are likely to see prices move higher for new crop peanuts.

Planting

Farmers planted without further contracting, and we’ll just have to see if those decisions were right or wrong depending on acres, yields and weather. What about total acres? Most buying points are reporting that farmers planted about the same as last year.

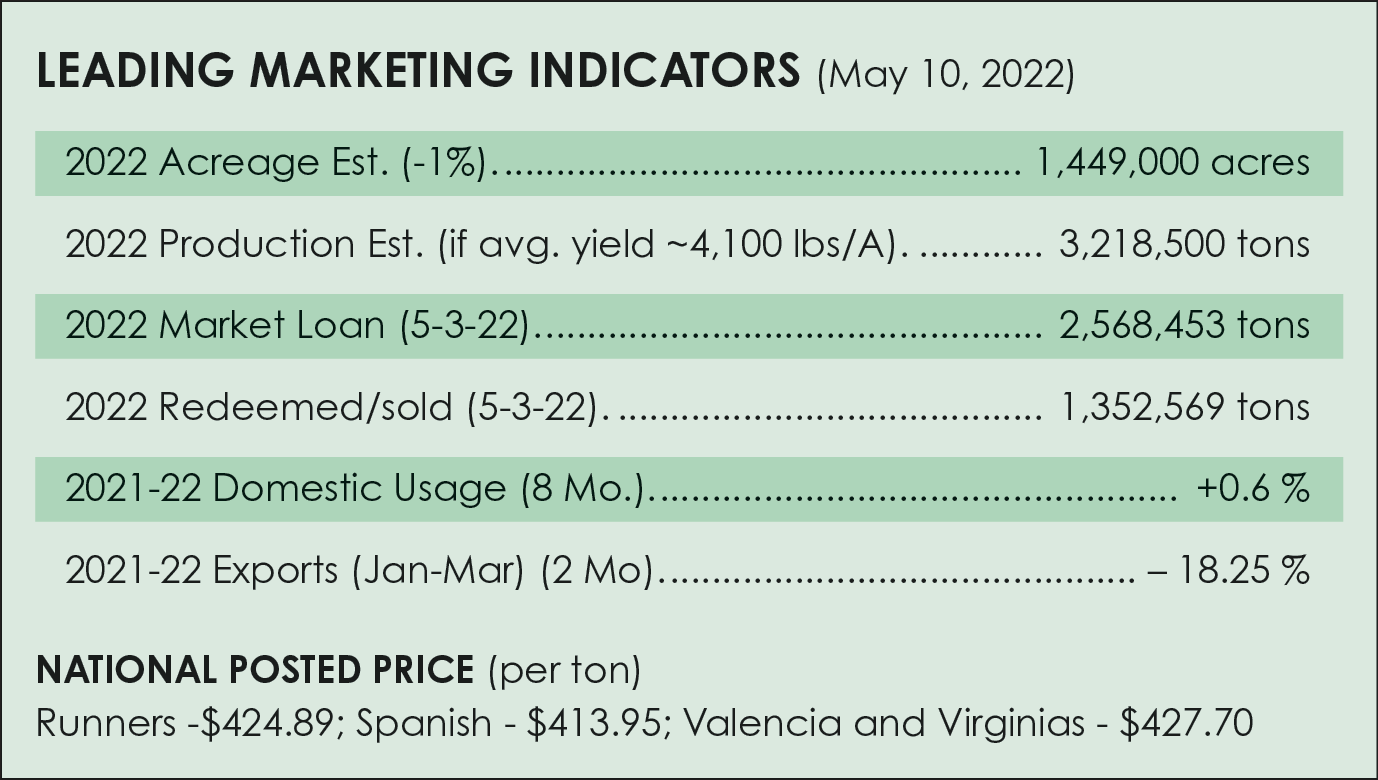

USDA estimates that growers intend to plant 1.57 million acres in 2022, down 1% from 2021. In Georgia, expected planted area is down 3% from 2021. Increases in planted area are expected in Mississippi, North Carolina, South Carolina, Texas and Virginia.

Average Price

A total of 1.57 million acres of planted peanuts with an average yield of 4,100 pounds per acre piles up 3.22 million tons of peanuts. Demand is estimated at 3.09 million tons and carryforward is expected to increase near 1.1 million next season. Even though cotton and corn are at record prices, it will take a drought or increase in demand to move the peanut market.

Shellers are caught in the middle. Farmers are sailing into unknown market territory with few contracts, but the market loan gives them some protection, especially those coupled with the price loss coverage program on base acres and any cooperative support from the previous year.

The average price of peanuts has pushed higher this year and is estimated by USDA at $484 per ton. Subtract the average price from the reference price of $535 per ton, and that yields a PLC payment of $51 per ton in October for the previous year.

Domestic Use

Peanut usage increased 0.6% during the past eight months for raw-shelled peanuts in primary products. Peanut butter is down 1.7% for the eight-month period, with a March 2021 versus March 2022 comparison down 5%. Candy was a winner in March up an amazing 30.4%. Snacks are down 4.3%, along with in-shells down 3.5% for the year, but a jump in March up 8.7%.

The market is strong, but the end of the pandemic and more eating out rather than at home is showing in peanut butter numbers. Talk of a food shortage could benefit peanut butter if consumers stock up. USDA predicts that domestic food use will rise only 1% for the year.

Exports

Peanut exports are predicted to decrease 12% this year. For the first two months, U.S. peanut exports are down 18.25% compared to the same period last year. Major purchases were seen in Mexico (+25%), The Netherlands (+300%) and Germany (+159%).

By category, peanut butter was down 2.9%, in-shells down 57%, with raw kernels up 9.72%. Heavy congestion exists in all European ports, which affects the supply chain. China is back in the market with a 15% market share behind Mexico and Canada. Peanut oil prices are expected to increase after the suspension of sunflower seed and oil from Ukraine and Russia.

Argentina is reporting more cold weather slowing the maturity of the peanut kernels. They are also noting a great concern that is developing into a severe situation…a serious lack of fuel for harvesting equipment and restrictions due to roadblocks. The EU continues to favor Argentine peanuts because of low or no aflatoxin.

Markets may be quiet at planting time; however, an estimated 50% of peanuts have not been contracted with shellers. There is a day coming that shellers and farmers must agree on some price or divert peanuts to the loan for a longer wait. There are many unknown issues that could influence the market such as inflation, cost of inputs, a labor shortage, a food shortage and the Farm Bill. Stay informed in case this quiet market turns to chaos.

{kind=link}