Contributing Editor

United States Representative Austin Scott, Tifton, Georgia, said it best, “The economy in rural America starts and stops with the American farmer. Amid the deafening noise inside political echo chambers and ceaseless squabbling of Congress is one truth that we cannot ignore — we are a nation united in reliance on our farmers.

“Without the American farmer, there is no adequate tax base for our school systems, local municipalities or any services that rural Americans need to live and prosper in this country. Everybody eats, and we all need the food and fiber that our farmers produce to live. No one wants to be dependent on foreign sources for food, just like no one wants to be dependent on foreign sources of energy. Right now, our farmers need our help.”

One-Year Farm Bill Extension

Those comments were delivered by Rep. Scott in the House Agriculture Committee, which earlier this year passed the Farm, Food and National Security Act of 2024 or their version of the Farm Bill. This legislation includes critical updates to reference prices and several priorities to ensure a strong farm safety net, such as expanding crop insurance options to specialty crops. Scott says all of these items would assist producers in times of natural disaster.

“However, the bill has stalled in Congress, and Senate Democrats recently released a half-baked, last-minute ‘Farm Bill’ just to look like they did something, further fueling the fear of the forgotten farmer as they struggle to feed us,” he says.

Perhaps his comments paid off as it spurred the U.S. House of Representatives to pass H.R. 10545 by a vote of 366-34, which included a continuing resolution for fiscal year 2025 appropriations funding, a one-year extension of the 2018 Farm Bill and $10 billion in agricultural economic assistance.

On the economic assistance segment of the bill, peanut producers can expect to receive an estimated economic assistance payment of $76.30 per acre no later than 90 days after the bill is enacted. That could be enough to help get farmers financed again. With the Farm Bill being extended, peanut farmers will have the $355 per ton loan available and the reference price of $535 per ton. The average price is expected to be $536 per ton resulting in no payment to peanut producers from the peanut program.

Crop Size And Quality

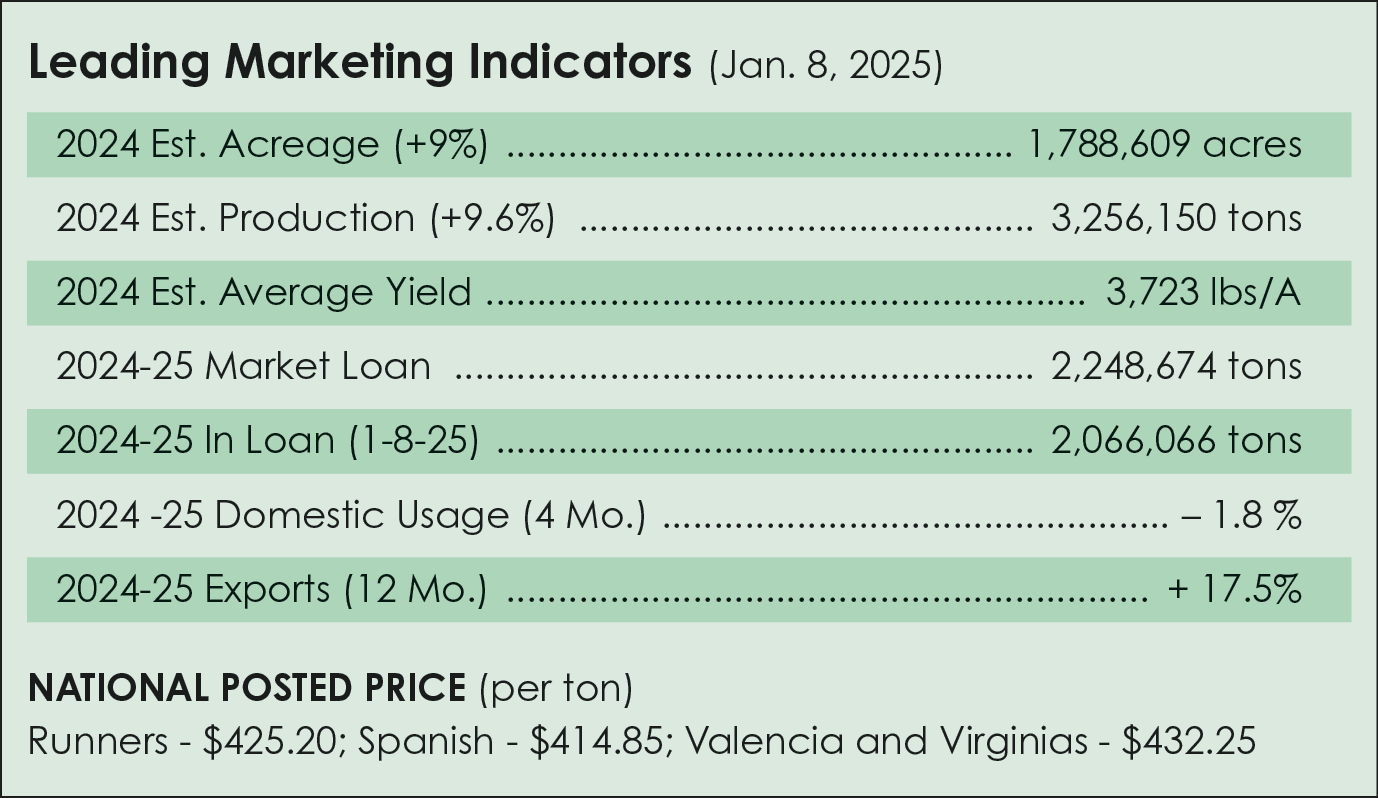

Production is estimated at 6.45 billion pounds, or 3,224,010 tons, up 8% from 2023. Planted area was 1.80 million acres, up 9%, and harvested area was 1.76 million acres, up 12% from 2023. The average yield is estimated at 3,668 pounds per acre, down 141 pounds from 2023. Record-high acres and production were achieved in Arkansas and record yields were estimated in North Carolina and Virginia.

Only 12,167 tons of Seg. 2s (0.4%) and only 4,514 tons of Seg. 3s would indicate crop quality is very good. Markets apparently needed peanuts as 20% went to commercial areas and 80% to the loan. Usually, an average of 10% goes directly to commercial markets.

Contracts were mostly $500 to $525 per ton on runners at planting time. With all the weather damage and drought, farmers thought the crop would be short and they could possibly pick up a premium on loan tonnage before next season. Most farmers sold loan peanuts for $550 to $575 per ton; however, that idea of a major premium never developed.

Still No Real Alternatives

All in all, it’s a very quiet market as far as trading goes. The crop continues to creep up in size, 3.186 million tons as of the latest report and will likely hit 3.2 million farmer-stock tons. Buyers seem content to wait before buying additional coverage. Increased plantings and decent rains in Argentina have their crop off to a good start, which adds to the buyer’s bearish mentality.

With weak competing commodities, like cotton at 68 cents per pound and corn at $4.50 per bushel, it appears peanut acreage could increase slightly for 2025. One broker said he imagines growers are hoping for a contract around $550 per ton and doesn’t think that’s a stretch.

Another broker reports that kernels are being indicated for the remainder of calendar year 2025 around 63 to 64 cents per pound, but buyers don’t seem too keen to buy at those levels today at least.

Domestic Markets

With commercial storage down about 3%, raw peanuts in primary products decreased 1.8% in August through November compared to the same four months of 2023. Peanut butter usage declined 3.1% compared to the previous year but bounced back by 3.6%. Candy usage is down 5.7% for the four months after a .4% decline in November versus last year. Peanuts in snacks are up 1.8% compared to last year.

Ending stocks this year are estimated at 811,000 tons. That means supplies will be tight, enough so to likely keep the price firm on shelled product, but also keeping farmer contracts above $500 per ton.

Export Markets

Export markets were up 17.55% in volume for the year, with 585,789 metric tons compared to the previous year’s 498,330 metric tons. President Trump’s tariff talk worries the peanut industry, especially in regard to shipments to our best customers Mexico and Canada.

Growing peanuts in 2025 will be a price agreement between the grower and sheller with advice from the buying point. A new, viable Farm Bill is not something you can count on and, for now, the extension will have to do. Manufacturers should be making sure peanuts are planted by booking at a price that will keep the farmer profitable. As we also learned this past season, you can wait too late to plant.

Support your farm and peanut leaders as they battle for your livelihood and agriculture as a whole.

{kind=link}