Contributing Editor

At a recent farm show, farmers were asking, “What are we going to do now?” Cotton and corn prices are lower than the cost of production. Soybean prices look better, but a farmer knows they are not good in a peanut rotation. The question they kept asking me — “What do you think peanuts will do in 2024?”

I don’t have the answer; it lies in negotiations between the farmer, the sheller and the financier. Most farmers are hoping that 2024 will be better than 2023. The 2023 crop was hammered with problems from start to finish but fortunately ended with a respectful number of total tons. Overall, yields and grades were down all across the peanut belt.

Tough Growing Conditions

In Georgia, peanut yields were down 1,500 pounds per acre in irrigated fields. Dryland fields were unusually mixed, some good and some bad. Grades were down with an average of 72.6. Almost 40% were below that average grade and only 19% were graded 76 or better. Season-long drought affected some areas this year, with West Georgia, Alabama and West Florida being the hardest hit, resulting in reduced yields and lower grades. Harvest conditions created more Seg 2s and Seg 3s. The eastern parts of Georgia and Florida fared better with higher yields and grades.

The U.S. peanut market is similar to last year and hard to describe. Shellers were cautious in the early season knowing that the crop was already in drought trouble and could be a disaster. Most of the shellers were only offering $525 per ton, but as harvest started, most added a $25 bonus per ton recognizing that production costs had increased. Shellers waited on a more definite account of the number of tons to be delivered and the shell-out quality as well.

Heat, Drought Affect Quality

Buying points reported that farmers thought the crop was short, and with costs increasing, uncontracted farmer- stock prices should have increased. Some buying points did offer $600+ per ton for farmer stock, mainly to match competing offers by other buying points. Some farmers optioned to place the peanuts in the market loan convinced that the prices would increase.

Shellers are reluctant to lock in large volumes without buyers. There are smaller-sized kernels and prices for larger grades that will maintain a strong premium throughout the season. One factor different from the year prior is overall quality is mixed and shellers will ask premiums for tight specs.

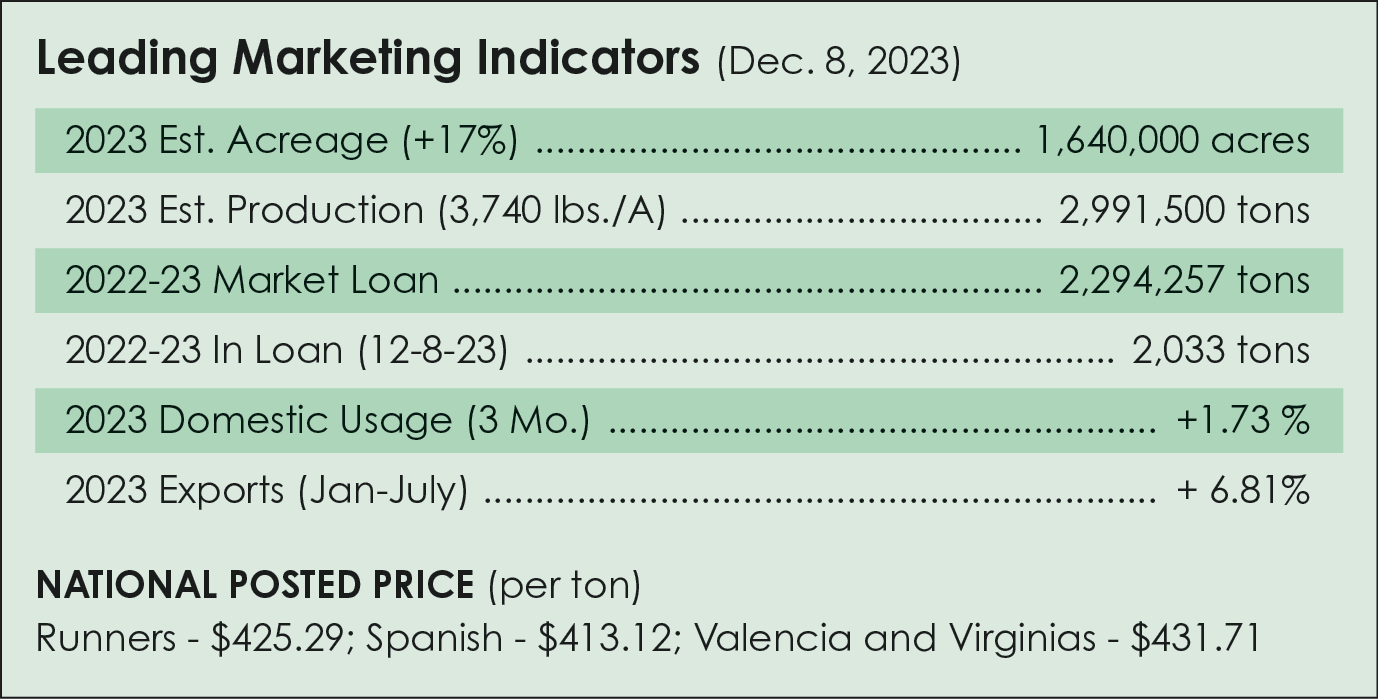

The Federal-State Inspection Service reports the total tonnage as of mid-December is 2.81 million tons, 94.2% of the November estimate of 2.99 million tons. The U.S. Department of Agriculture predicted the 2023 peanut yield at 3,740 pounds per acre, down from 2022’s 3,905 pounds per acre. Harvested acres were unchanged from earlier estimates at 1.6 million acres, up 16% from the previous year.

With a lower peanut production forecast, total peanut use is reduced by 150 million pounds with peanut crush down 50 million pounds and exports down 100 million pounds. Ending stocks are reduced by 114 million pounds to 1 million tons, similar to 2022.

Domestic Use

The good news from USDA is their report showing domestic food usage is up 3.7%. Exports are also up 4.5%. Ending stocks of 1.01 million tons will remain the same as last year.

Raw peanuts in primary products are up 1.73% compared to August-October 2023. Peanut butter continues to set new records with volumes of raw shelled, up 4.8%, an increase for the three-month period compared to the same three months last year. Peanut use in candy and snacks is about the same as last year.

Export Markets

U.S. peanut exports for the year through July increased 6.8% by volume. Total exports reached 316,283 metric tons, valued at $489 million.

Mexico remains the top international market for U.S. peanuts, with shipments increasing 0.4% by volume to 88,134 metric tons. China surpassed Canada as the second-largest importer of U.S. peanuts. Drought in Argentina and Brazil will reduce their exports, leading to more inquiries of U.S. shellers to possibly supply product.

Reasons For Optimism

One factor to watch in peanut markets is the Price Loss Coverage payment from the peanut program. USDA says that the effective reference price for peanuts is $.2675 per pound or $535 per ton. The market price average of $540 per ton is deducted from the reference price of $535 per ton, but that’s a negative number, meaning the PLC payment for 2022-2023 is $0. The U.S. Peanut Federation has been pleading with Congress to increase the reference price; however, the response has been, “No new funds are available.”

The peanut industry is in a pretty good position with prices high enough to hopefully offset increased costs. Scientists report that new varieties are being introduced with some levels of resistance to leaf spot, nematodes, white mold and tomato spotted wilt virus, some that may even yield 7,000 pounds per acre. That’s a reason to feel optimistic about the future.

Georgia Grower To Chair APC Board

The American Peanut Council elected a new chair at the organization’s annual Insights Summit conference in Washington, D.C. Georgia grower Donald Chase, owner of Chase Farms, will lead the APC board of directors for the 2024 term.

Chase, together with his wife, Michelle, and parents grow peanuts, corn and sweet corn on 600 acres of irrigated land. Chase Farms also produces poultry.

“We are thrilled to have Donald at the helm of APC’s board of directors,” says APC President and CEO Richard Owen. “He is highly respected in the industry and is always looking to the future and how we can better the peanut industry to lower cost of production and improve sustainability.”

Chase is on the Georgia Peanut Commission, other peanut organizations and the Flint Energies board. He is the immediate past chairman of APC’s sustainability committee and vice chair of APC’s Board of Directors. He received his undergraduate degree from Southern Adventist University and an MBA from Vanderbilt University.

{kind=link}