Contributing Editor

Farmers usually get excited about this time of the year. The smell of the fresh-turned dirt brings back the good old days when the forefathers felt that production of food, fiber, fuel and shelter were all positive goals that united the family and preserved America’s future.

Gradually, things have changed. Excitement and optimism are dimmed by various problems, and farming becomes about survival. Production costs, inflation, international issues including the war in Ukraine, tariffs on our products increasing the price, cost of fertilizer, water wars, lack of border security, weeds becoming herbicide resistant, an increasingly complex global regulatory environment and climate change…all combine to dampen optimism.

Prices for gas and diesel have risen of late but are expected to decline about 2% in 2024. Any competing crops continue to have low prices and are at or below cost of production. Decisions on what to plant can only wait so long.

Peanut producers have listed some major concerns for the 2024 crop including early contract prices, cotton and corn prices stalled at or below cost of production, a serious drought in the Southwest growing area and unexpected weather in the Southeast. Wet, cool conditions through mid-April will push planting further into the spring. Planting too late can spell trouble with Tomato Spotted Wilt Virus. Producers also struggle to keep up with the U.S. Environmental Protection Agency’s regulations and the court’s revoking of rules, as in chlorpyrifos tolerances and Dicamba use in cotton. Production costs, pest and disease problems, nematodes, hurricanes and harvest weather – the list of real concerns goes on and on.

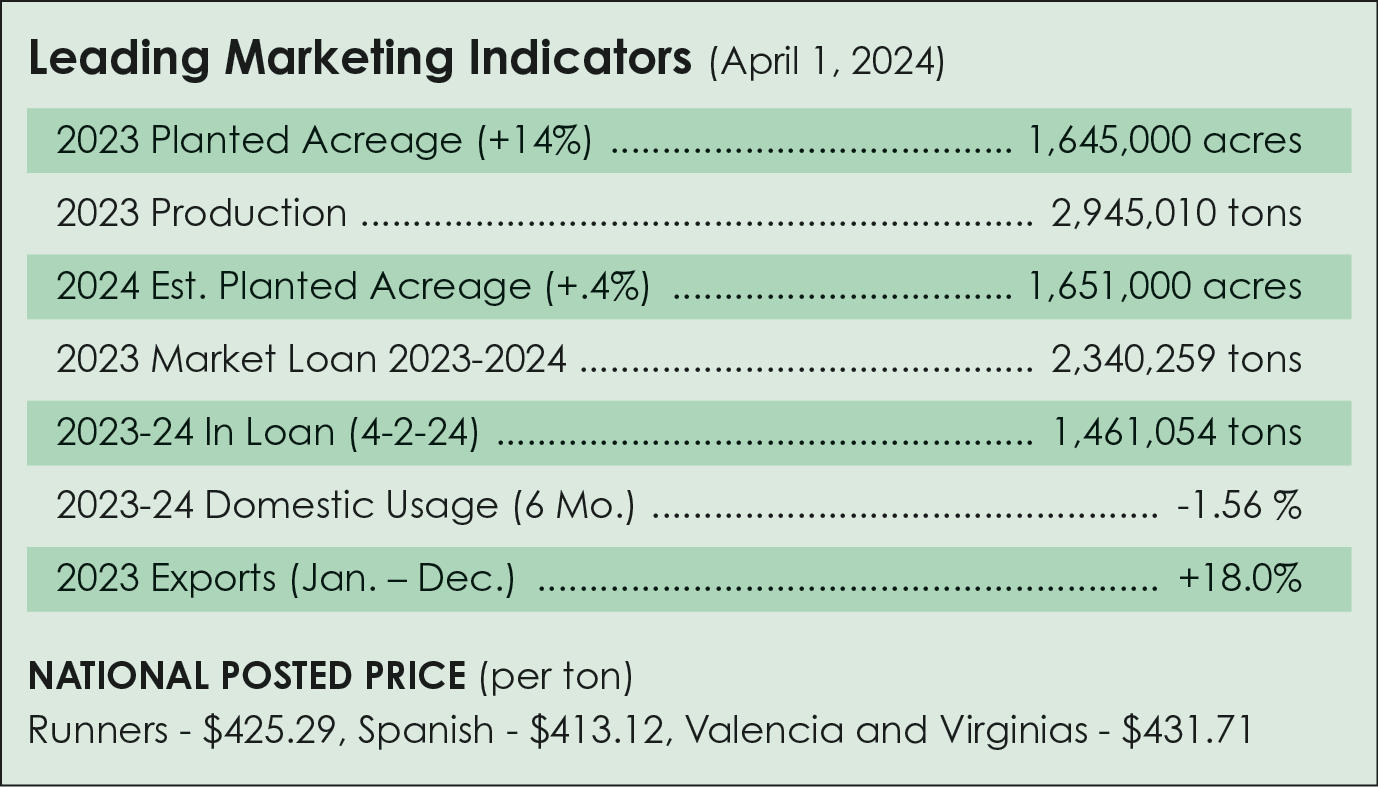

Planted Acres

The U.S. Department of Agriculture’s National Agricultural Statistics Service projects 1.65 million acres will be planted to peanuts in 2024, a less than 1% increase from 2023. That was somewhat of a surprise as other estimates have ranged from a 5% to 7% increase. Georgia, the largest-producing state, is projected to plant 820,000 acres, an increase of 5.8% from last year.

Southeast acreage is projected to be 1.24 million acres, up 7.2% from last year. In the Southwest, peanuts are projected to be planted on 175,000 acres, down 30% from 2023. However, some West Texas growers have indicated they are likely to plant about the same amount as last season and did not agree with the estimated 30% reduction. The outcome in this area will depend on further drought or recovery.

In the Virginia-Carolina area, peanuts are projected to be planted on 229,000 acres, virtually unchanged from 2023.

Farmer-Stock Pricing

In the Southeast, buying points report that shellers are offering a contract for runner-type peanuts for 2024 at $550 per ton for high-oleic peanuts and $535 per ton for non-high oleics. Tonnage is limited for each buying point. There are some perks such as $25 per ton for irrigation. Some shellers are not buying high-oleic varieties but are matching the price for regular oleics. Some buying points report good response, while others say farmers are still watching cotton and corn prices.

In the V-C region, buying points report contracts were being offered at $525 per ton for runner-type peanuts, $550 per ton for high oleics and $545 per ton for Virginia type. In the Southwest, runner-type contracts are $625 per ton and Virginias are at $675 per ton, all on limited acres with water. A rain is needed before farmers can plant.

The near market remains very firm, difficult to get offers and prices in the high $.60s and low $.70s, depending on grade and specifications. New-crop buyers are convinced there will be more peanuts planted in ’24 so they are looking for offers in the mid $0.50s to make a trade on the 2024 crop.

Buyers are hopeful new-crop pricing has room to move downward with an acreage increase, but that has not happened. With Argentina’s 2023 crop having major issues and the U.S. crop having less-than-optimal yields and maturity, the result was a big increase in U.S. exports of the remaining 2022 crop that was an excellent quality. Argentina appears to have a great crop coming in this season and will likely return to being the preferred origin for European Union imports. Brazil could have issues with their crop, particularly from aflatoxin.

This has left us with a projected carry-out below one million metric tons headed into the crop harvest this fall. Despite all the EU buying interest, the market was fairly slow to react in part due to the planted acreage report and a prolonged period with few domestic trades. Pricing rose into the mid $.60s per pound and has settled now where it currently sits.

Domestic Markets

USDA is reporting raw-shelled peanut usage down 1.56% for the six-month period in primary products with peanut butter showing an increase during the period of 1%. Peanut candy took a major fall in January; however, usage was down only 1.2% for the six months. Snacks were down 11% for the year. USDA’s summary showed usage of shelled edible peanuts down 2%.

In a major victory for peanuts, the U.S. Food and Drug Administration approved Xolair (omalizumab) to be used for reducing allergic reactions to multiple foods after accidental exposure.

Export Usage

On exports, 85% of U.S. peanuts currently go to mature markets. Market shares show China with 14%, Mexico with 29%, Europe (excluding the United Kingdom) is 20%, Canada with 25% and Japan with 3%. The next step change in U.S. exports will need to come from new categories in existing geographies or new geographic markets. The United States is not seen as a consistent supplier to Europe, which is conditioned for Argentina flavor/texture. Future U.S. import share to Europe is limited.

Competitiveness outweighs most marketing factors in a majority of export destinations. In an increasingly complex global regulatory environment, the U.S. peanut industry needs to be fully engaged in dealing with trade and technical threats, including aflatoxin, CODEX, a set of internationally adopted food standards, and much more. The American Peanut Council’s new market development process targets one new market per year.

Farm Bill Limbo

The Farm Bill and, therefore, the peanut program, remains unsettled. Farmers continue to plead for an increase in the reference price. If increased, it would be 2026 before farmers receive a price loss coverage payment. The search for funding continues, with suggestions ranging from using Commodity Credit Corporation funds, to unused climate change or COVID-19 funds.

Check with your buying point and sheller as there is time to change your 2024 plans. The industry needs and wants a good quality, plentiful crop. You deserve a profit, and buyers are willing to pay to keep you in business. Even with the many concerns, 2024 should be a good year for peanuts.

{kind=link}