Contributing Editor

As farmers approach 2024 planting season, most are hoping it is not similar to the 2023 season. Peanut production this past year had numerous events, many of which could not be explained. From the cold soils affecting seed emergence to constant record-breaking heat and a lack of rain in critical times, it seemed that the crop was always under stress.

As the crop developed, peanut production issues were different not just state-by-state, but also by county and even field-by-field. While the nebulous “normal” may not actually exist, should the crop be this varied even on the same farm?

Reduced Outcome Of 2023 Crop

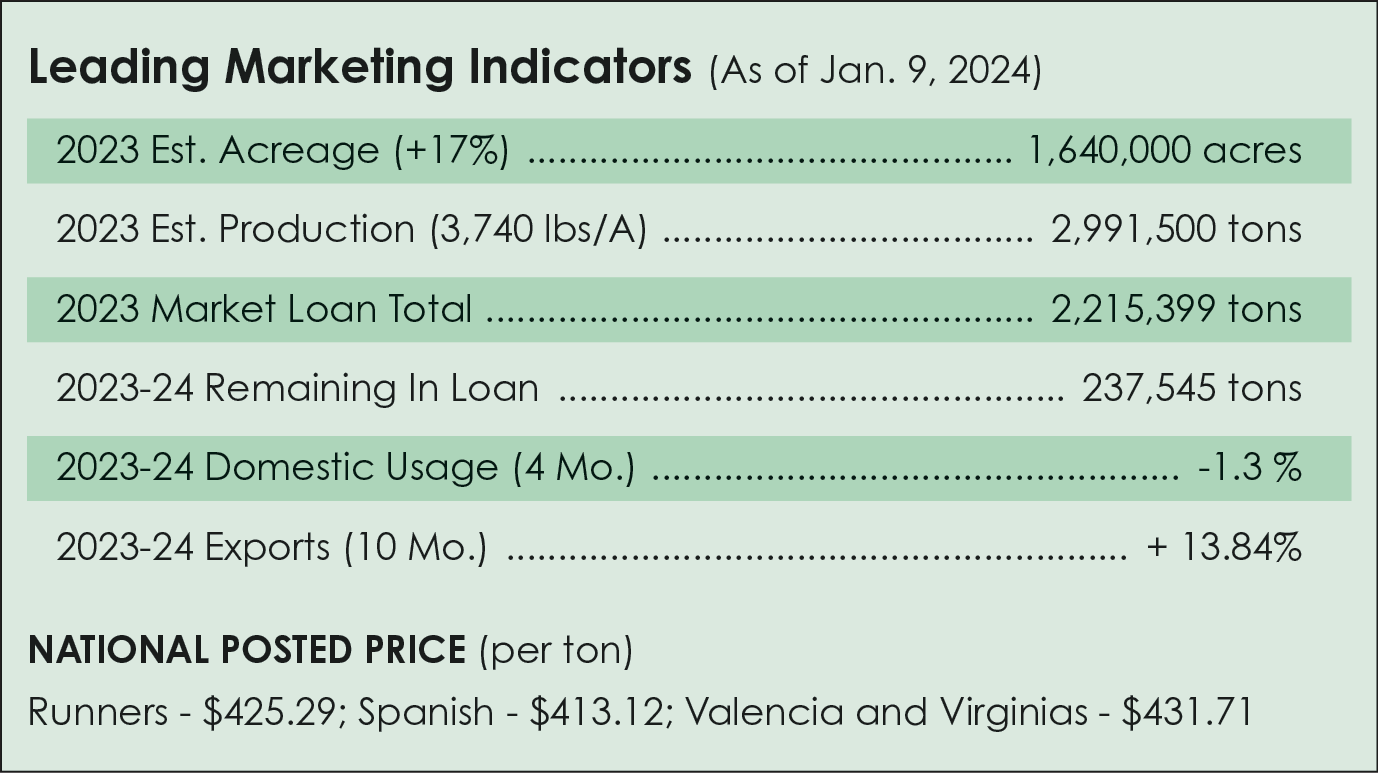

The market knew before harvest that it would be difficult for U.S. growers to achieve a 3.1-million-ton crop given the growing conditions that the crop endured in August. The end result was a 2.9-million-ton crop with quality that was less than ideal. The market firmed with higher specifications and higher prices for runners.

Offers on Virginia-type peanuts have been easier to obtain, both from in-shells and kernels. The issue with runners has impacted Virginia kernels as buyers make exceptions or look for alternatives. Blanching slots remain extremely tight, and blanched jumbos are pricing in the low 80 cents per pound, with blanched splits in the high 70 cents per pound if you can find them.

Will Peanut Be Priced To Plant?

Producers were already asking shellers for higher contracts because of the increase in the costs of production. As shelled peanut prices increased, producers wanted another boost. Some shellers added a $25 per-ton bonus. Many producers decided to place un-contracted tonnage in the government loan for $355 per ton hoping prices would increase before the sheller needed them in the market. With shelled runners offered at 70 cents per pound plus, farmers were being offered $625 to $650 per ton.

What about the 2024 crop? Producers must check in with their sheller/buying point to get an offer. Shellers have to check with manufacturers to get an estimate as to the volume and quality needed and the estimated price they’ll pay. Then, the sheller has to convert offers into farmer-stock contracts, finally making an offer to the farmer to grow the needed peanuts this season. Keeping in mind, costs of land, equipment and financing, farmers must decide how many peanuts to plant.

Are There Any Alternatives?

What about competition for crop acres? Cotton prices are moving parallel at 80 to 82 cents per pound. Corn is being offered at breakeven prices of $4.54 to $5 per bushel as a drop in fertilizer prices might encourage more corn acreage. Soybeans can be contracted for about $14 per bushel as stocks are the lowest in eight years. However, soybeans are not a good rotation crop for peanuts. With runner-type peanuts in the range of $500 to $525 per ton, all of these are below the cost of production.

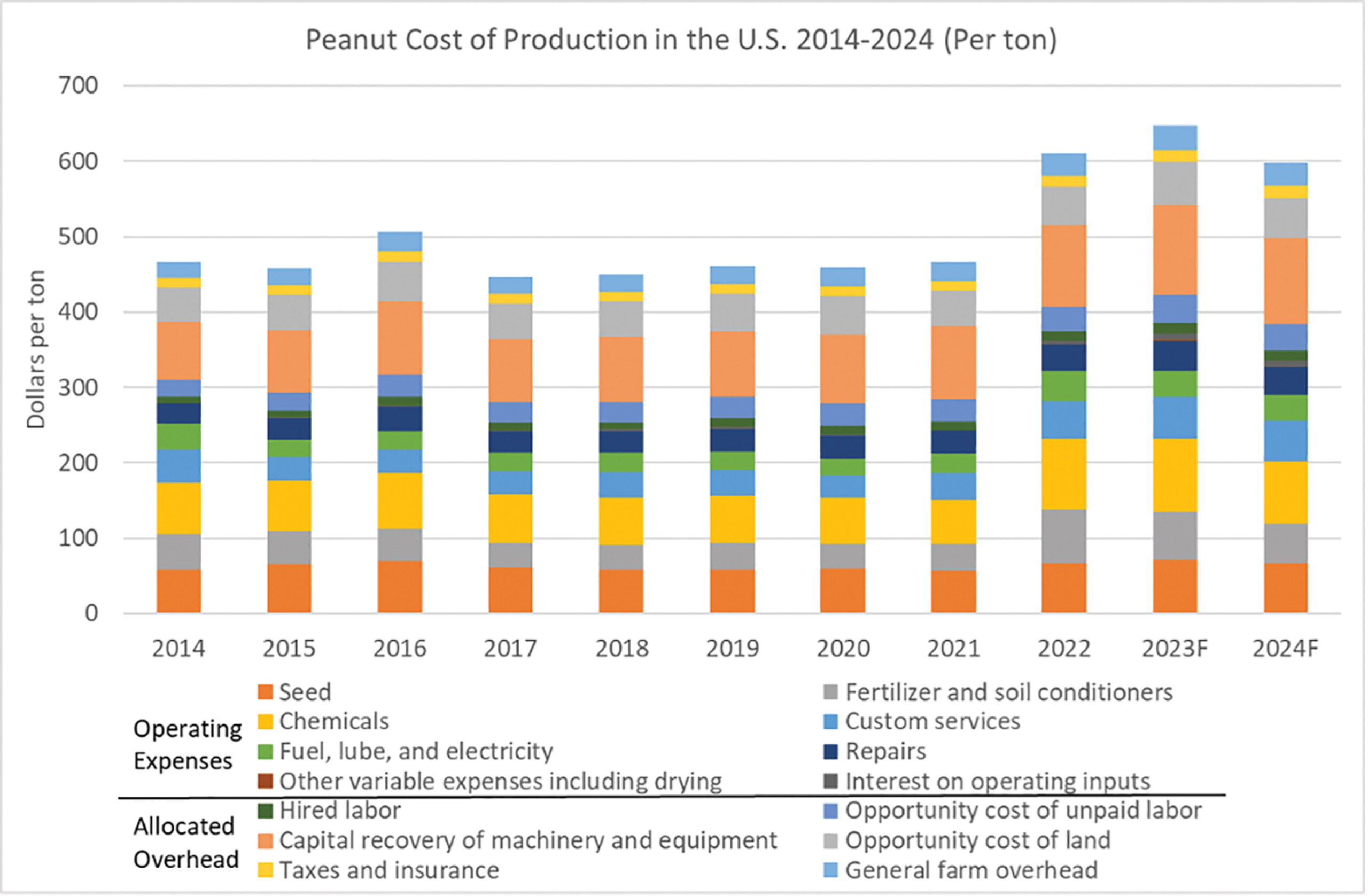

You can read about the projected cost of production rates from Auburn ag economist Adam Rabinowitz on the following page. However, the gist of it is that the total cost of production forecasted for 2024 is $598 per ton, a 28% increase from 2014.

USDA reports that the average price received by farmers for peanuts was 29.5 cents per pound or $590 per ton in November. The October average market price was 26.7 cents per pound or $534 per ton. The peanut program is designed to assist farmers with a Price Loss Coverage payment when the price received is below the reference price of $535 per ton. The average will be higher than the reference price; therefore, no PLC payment will be offered.

Domestic Markets

Peanut Stocks and Processing is reporting peanut usage down 1.3% for the four-month period for raw peanuts in primary products, with peanut butter showing an increase during the period of 1.6%. Comparing November 2022 with the same month in 2023, peanuts in candy decreased 17.8%, snacks were down 13.5%, peanut butter was down 7.6% and in-shells were down 10.7%. USDA says overall peanut usage is down 1% from the past year.

Exports

U.S. peanut exports for the year-to-date through October increased 13.84% by volume compared to the same period in 2022. Total exports reached 462,421 metric tons, valued at $729.7 million.

Mexico remains the top international market for U.S. peanuts, with shipments increasing 7.07% by volume to 132,342 MT. Mexico, Canada and China are 70% of the U.S. exports.

Peanut industry leadership continues to campaign for an increase in the reference price to offset increases in production costs. The government loan program will clear out the 2022 crop with all peanut loans repaid for the second year in a row. That’s good news is you’re talking with your Washington D.C. representatives.

Cost Of Production, The Farm Bill And Need For Risk Management

Marketing peanuts can be challenging for producers because of a lack of a futures market and relatively concentrated first buyers. This makes it more important for producers to evaluate their cost of production to help control input costs and make strategic risk management decisions.

According to the USDA Commodity Cost and Returns for peanuts, cost of production increased in 2022 and has stayed at this higher level, like other commodities. The chart shows the 2024 forecasted operating cost of production at $336 per ton. This covers seed, chemicals, fuel, repairs and interest.

Allocated overhead includes general farm expenses that are allocated to the peanut operation, such as labor, the cost of machinery and the opportunity cost of land. When including allocated overhead, the total cost of production is forecasted for 2024 at $598 per ton, a 28% increase from 2014. These costs are slightly lower than the $648 per ton total cost peak forecasted for 2023, but nowhere near the levels seen in earlier years.

In a “Southern Ag Today” article Dec. 4, 2023, it was shown that peanut prices are continuing to rise since the low in 2015, and USDA expects prices to be about $550 per ton for the 2023-2024 marketing year. This is still below the cost of production shown on the chart.

The Farm Bill is a safety net for producers with base acres through the ARC/PLC and marketing loan programs, but price levels have not changed since the 2014 Farm Bill. For the PLC program, the reference price is $535 per ton. While the 2018 Farm Bill allowed for an escalation through the effective reference price, that has not triggered for peanuts. Meanwhile, the marketing loan has been set at a rate of $355 per ton. This does not provide a safety net for these higher costs.

While Congress continues to debate the Farm Bill, producers need to look at alternative marketing strategies and other ways to help mitigate the rising costs of growing peanuts. Cross hedging is a popular marketing strategy used to mitigate risk, but there is little empirical evidence that it is effective for peanuts. That leaves contracting, cost control and crop insurance as the most viable risk management tools for peanut producers.

{kind=link}