Contributing Editor

T

he peanut market starts 2023 in an unusual position with fewer peanuts produced. Anytime there is a shortage, or even a rumored shortage, prices trend higher. The peanut producer wants to price peanuts when it reaches its peak. The manufacturer wants a reasonably priced and quality product while paying the same price for raw materials as the competition.

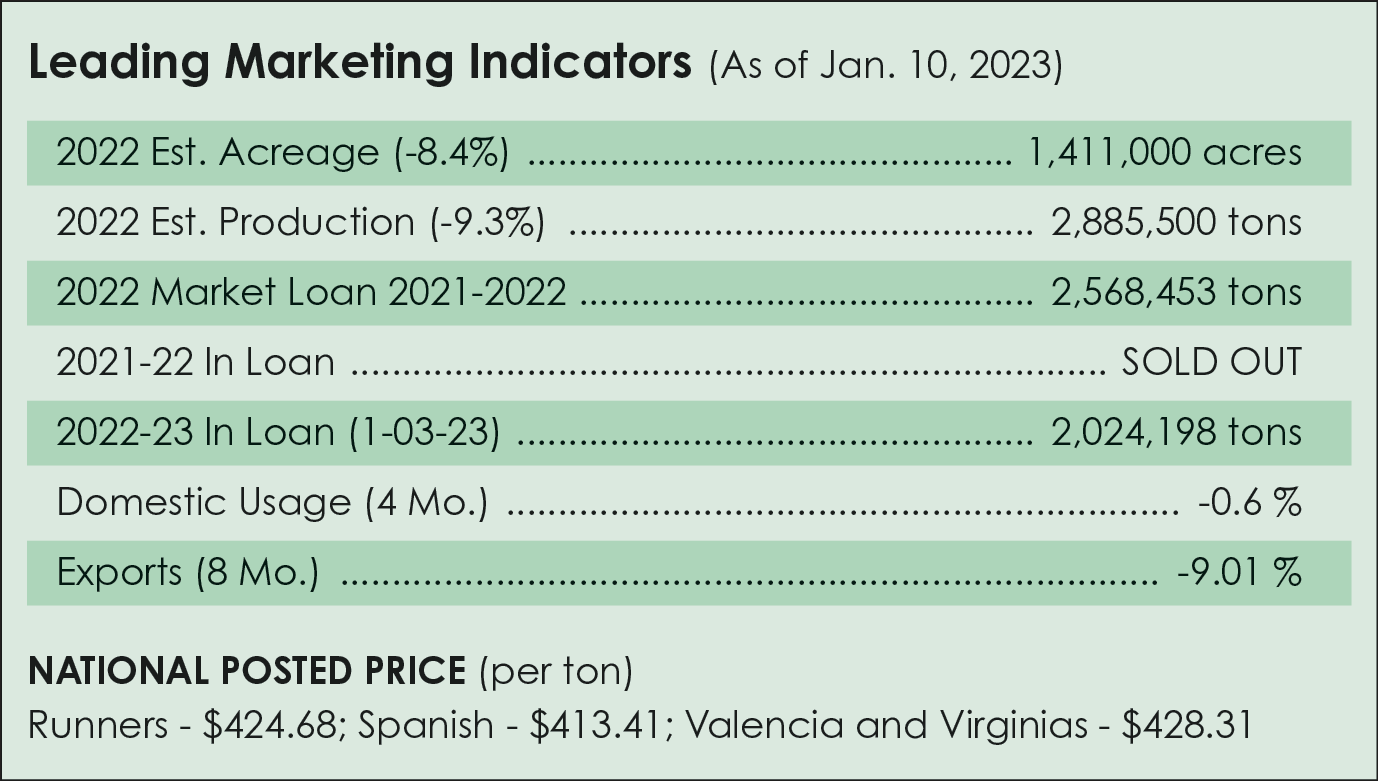

Federal-State Inspection Service has recorded a total of 2,764,389 tons inspected at peanut buying points for the 2022 crop as of Jan. 6, 2023. That is 121,000 tons short of the U.S. estimate and 416,276 tons fewer than last season – a 13.1% drop in farmer-stock peanuts and not an insignificant amount.

Domestic Shortfall

More than 250,000 tons have been purchased directly from farmers and classified as commercial ready for processing. Another 1,700,000 tons are stored as a loan, with 806,000 classified as receipted.

In 2022, acreage was down 8.5% as cotton prices soared and competed for the land. Shellers had to pay higher contract prices to make sure enough acreage was planted. Costs were rising, and inflation was rampant. Manufacturers tried to cover their needs at a reasonable price before prices moved any higher.

Some farmers rejected the $500 per-ton price offer and chose to wait. Shelled prices continued to rise, and most producers who decided to wait finally accepted $600 to $650 per ton and even some at $700 per ton. While 2022 was the year to wait, it often pays to average it out in the long run. When a profitable contract is offered, and it might go higher, book some, then wait and book some more later, or option for the sheller/farmer pool and ride the market up.

Price Increases

After harvest has ended for the farmer, the sheller is busy shelling and selling. Most of the peanuts were sold earlier based on the early farmer-stock contract of $450 to $500 per ton. Raw-shelled peanuts for runners have increased from 53 cents to 55 cents per pound to today’s 62 cents to 66 cents per pound. The perceived shortage is pushing prices higher, yet most of the peanuts were delivered at the lower prices.

Producers and buyers will be pricing and sharing the sales for over a year. A sheller recently announced a payout of $22 per ton, over and above contracts and other premiums from seed or irrigation. A new ReGeneration cover crop program will net the farmer another $10 per acre. With higher-shelled prices, sheller/farmer pools should pay a premium or bonus above the basic contract. Co-ops have another economic strategy to pay dividends during the year after peanuts are sold.

Because farmer prices have been so low, the Price Loss Coverage program has paid out to the farmer. The PLC payment is determined by subtracting the annual average price from the reference price. Last year was more than $40 per ton. Because of the higher average price received by farmers, the PLC is estimated at $5 per ton paid in October for last year. Because of higher costs, the reference price needs to be adjusted upward in the new Farm Bill.

Positives In The Market

The market has some positives that merit a mention. The market loan from 2021-2022 redeemed 2,568,453 tons, which entered the market and did not have to be bought by the government. That is good news. Per capita consumption and total peanut consumption are at record levels. The U.S. House of Representatives Appropriations Committee has approved more than $4 million in FY 2023 spending to mitigate aflatoxin in peanuts.

Another positive is approval of $2,498,000 for the American Peanut Council in Market Assistance Program funding, plus another $470,000 for Foreign Market Development to promote peanuts and peanut products in selected markets in 2023. The Peanut Institute continues to publish research that shows peanuts improve heart health and blood sugar, protect against certain cancers such as colorectal, gastric, pancreatic and even lung cancer and improves your chances of living longer.

The quality of the 2022 crop is another plus.

Watching The Cotton Market

All that is good, but what will peanuts bring this spring? Cooperatives will likely offer a lower front-end contract with another payment likely in October, and then a payout next year. With higher average prices, the PLC is no help.

If buyers refuse the higher-priced shelled peanuts, the sheller has no choice but to wait on the farmer to negotiate with the sheller on a 2023 peanut contract. Industry cannot wait until planting time because cotton contracts may go to $1.30 per pound again. Farmers tell me that if cotton is 80 cents per pound, they would plant peanuts. Don’t wait too long.

Another silent factor is China. In 2021, China bought over 200,000 metric tons. With higher prices, it will not likely happen this year since the United States has fewer Seg. 2 or Seg. 3 lower-priced peanuts to sell. At one point, China was buying 40% of the U.S. exports.

The peanut market summary is essentially the same as last month. The market is quiet as buyers have good coverage and are not wanting to buy into the market at the prices it would take to find a willing seller. For now, we watch cotton and China, and pray for rain. Industry supply seems adequate but will need an increase in acres in 2023. How do we get this outcome if manufacturers don’t want to pay? PG

{kind=link}