Contributing Editor

The peanut industry is running under caution, and peanut farmers are worried that during the caution, the next wreck could take him or her out. Around every corner are potential problems from an early lack of rain, everything costing more, contracts being reduced below the cost of production, Trump announcing tariffs on our best markets, prices on alternative crops that are worse than peanuts, no Farm Bill help from the government and the list goes on.

While talking to a farmer about his plan for this season, he commented, “Call me back when I have a better attitude.” Another farmer was asked what he would advise, and he said, “Don’t farm!”

Hopefully, things are better in some areas, but as some also commented, it could get worse before things get better. President Trump pledged strong support for farmers in his Report to the Nation speech. Newly confirmed Secretary of Agriculture Brooke Rollins pledged to get economic assistance payments to farmer’s farm accounts through the Farm Service Agency by planting time. For peanuts, the estimated assistance payment of $76.30 per acre is the peanut part of the $11 billion package.

Crop Value And Contracts

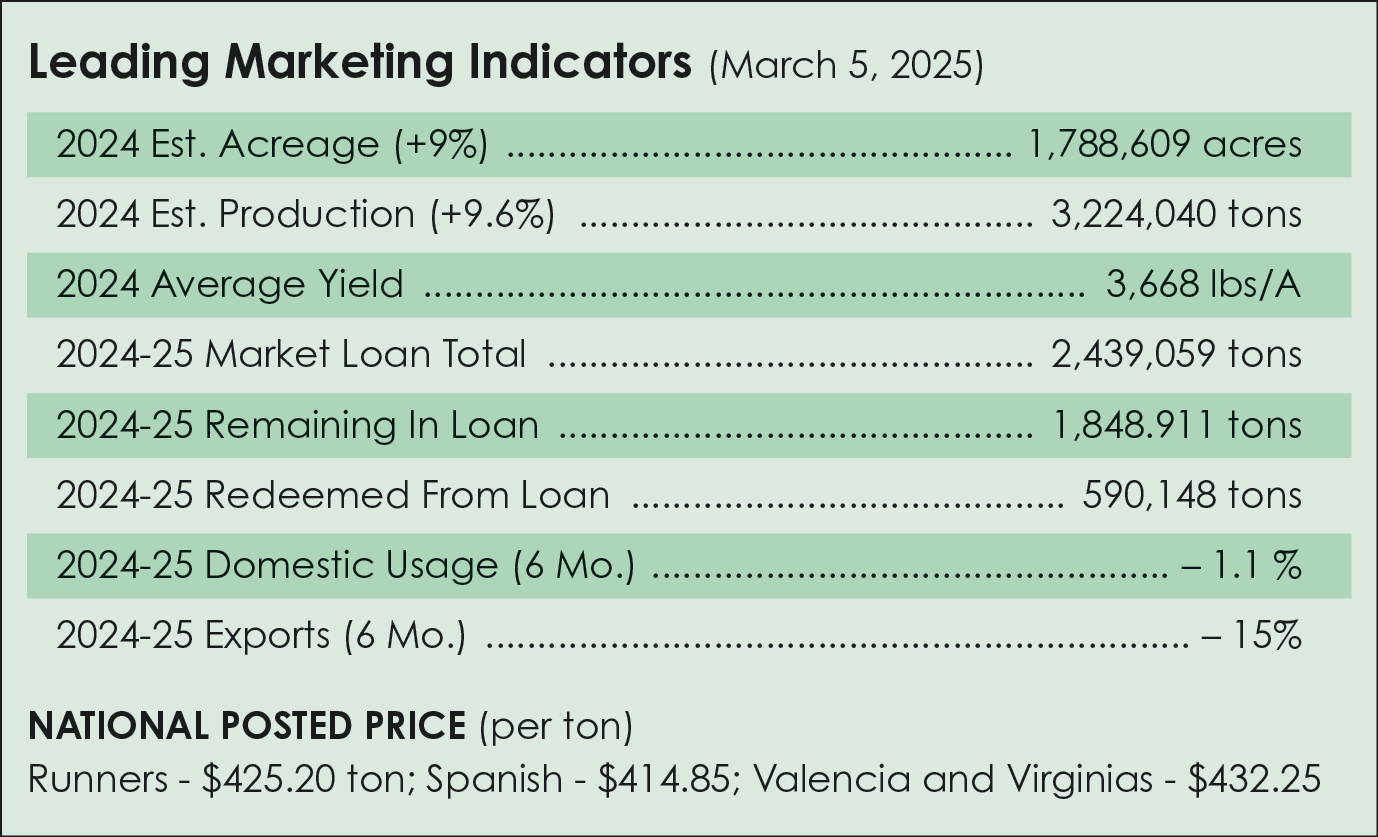

The Farm Bill has been extended until Sept. 30, 2025. The industry still has the $355 per-ton loan available and the reference price of $535 per ton. The average price is predicted to be $536 per ton resulting in no payment to peanut producers.

The farm-gate value from the U.S. Department of Agriculture’s National Agricultural Statistics Service for the 2024 crop was $1.6 billion, 4.6% more than 2023’s value. The average price in 2024 was 25.8 cents per pound or $516 per ton. That compares to 26.9 cents per pound in 2023 or $538 per ton. The average price in Georgia was $482 per ton. The highest price per pound was Texas at 37.9 cents per pound or $758 per ton. Oklahoma was second at $612 per ton. The lowest price was in Alabama at 23.6 cents per pound or $468 per ton.

For 2025, the Southeast’s peanut buying points reported by mid-February that peanut contracts for runner-type peanuts at $500 per ton were open. The contract is limited to half of the farmer’s production in 2024. Shellers are reportedly matching the offer if the farmer is ready to sign. Reports indicate a good response; however, farmers were critical of limits. Contracts were available at $605 per ton for Virginia-type peanuts, again with limits, and even some $525 per-ton offers for high oleic varieties. Don’t look for any new contracts until after planting.

Tariff Trouble

When the Trump Administration announced the 25% tariffs on Canada and Mexico and a 20% tariff on China, all sheller contracts were pulled and no longer available. What’s next? Nobody knows. With cotton at 63 cents per pound and corn at $4.20 per bushel, farmers are likely to increase peanut acres. Leaders are warning farmers not to overplant. The danger with growing peanuts is that the recipe for quality production requires crop rotation, approved herbicides and insecticides, fertilizer, calcium and quality certified seed and water, especially at pegging time. To vary from the recipe jeopardizes the total production and final quality of the peanuts.

The domestic market for peanuts and peanut butter is considered cautiously calm knowing product is available from the 2024 crop, and with the expected acreage increase, prices should remain about the same or lower.

Domestic Markets

Raw peanuts in primary products are down 1.1% from August to January compared to the same six-month period of 2023. Peanut butter usage dropped 7.6%, pushing the six-month volume down 2%. Candy usage is down 7.2% for the six months after a 5.5% decline in January versus last year. Peanuts in snacks are up 8.7% from January to January and are now up 4.6% for the six months.

Export Markets

Export demand for peanuts and peanut products has declined 14.91% over the first five months of the marketing year compared to the previous five months. Canada has reclaimed the title as the top U.S. market while Mexico drops to second and China third. Exports to China and the European Union declined significantly in the past year. China is a major peanut producer and reduced demand for peanut imports last year because of their record crop.

For the European Union, difficulty in meeting the EU’s strict aflatoxin limits curbed U.S. peanut butter exports to the region as increased screenings in the past led to rising import costs. This is especially an issue for consumer-ready products as the permissible levels for the EU are more restrictive than for the United States. The American Peanut Council’s market development programs are expanding and will include the Market Access Program, Foreign Market Development Program and the Regional Agricultural Promotion Program.

Balancing Supply And Demand

Planting too many peanuts this year, given good rains and a favorable season, means an over-supply next year. Farmers know the right thing to do is to stay with their rotation and avoid planting peanuts behind peanuts. Be conservative and do your part in balancing supply and demand. We are fortunate to have a good domestic market, down only 1%, and an export market that has promise with more promotion.

If you cannot find a profitable contract, place peanuts into the loan at $355 and wait.

{kind=link}