Contributing Editor

The peanut market is very quiet. Currently, raw-shelled peanuts are available from 68 to 72 counts, and buyers come in as needed for spot sales. The market seems to believe that supplies will be below average causing the price to remain higher than normal.

Some coverage was needed through the summer, but buyers think markets will weaken as the planted crop germinates and progresses. Any prolonged dry weather from June forward will push new crop prices higher from the current 59, 58 and 57 cents per pound for jumbos, mediums and splits, respectively.

A 3.1-million-ton crop of good quality peanuts is needed as carryover from the 2023 crop will be below historic levels. Many buyers have taken some coverage on the new crop and are now in a wait-and-see pattern until the crop is planted and begins progressing.

With the anticipated short supply and higher costs of production, contract offers were above the $500 to $525 per-ton level for Southeast and Virginia-Carolina runner-type peanuts. Virginias were also higher in the V-C area and in the Southwest. Some buying points reported heavy action, especially if a sheller/buying point pool was an option offering hopes that the price would be higher later.

Buyers continue to point to cotton prices at 75 to 80 cents per pound as the reason there should be an increase in peanut planting and, therefore, lower prices for raw-shelled kernels.

Planting Intentions

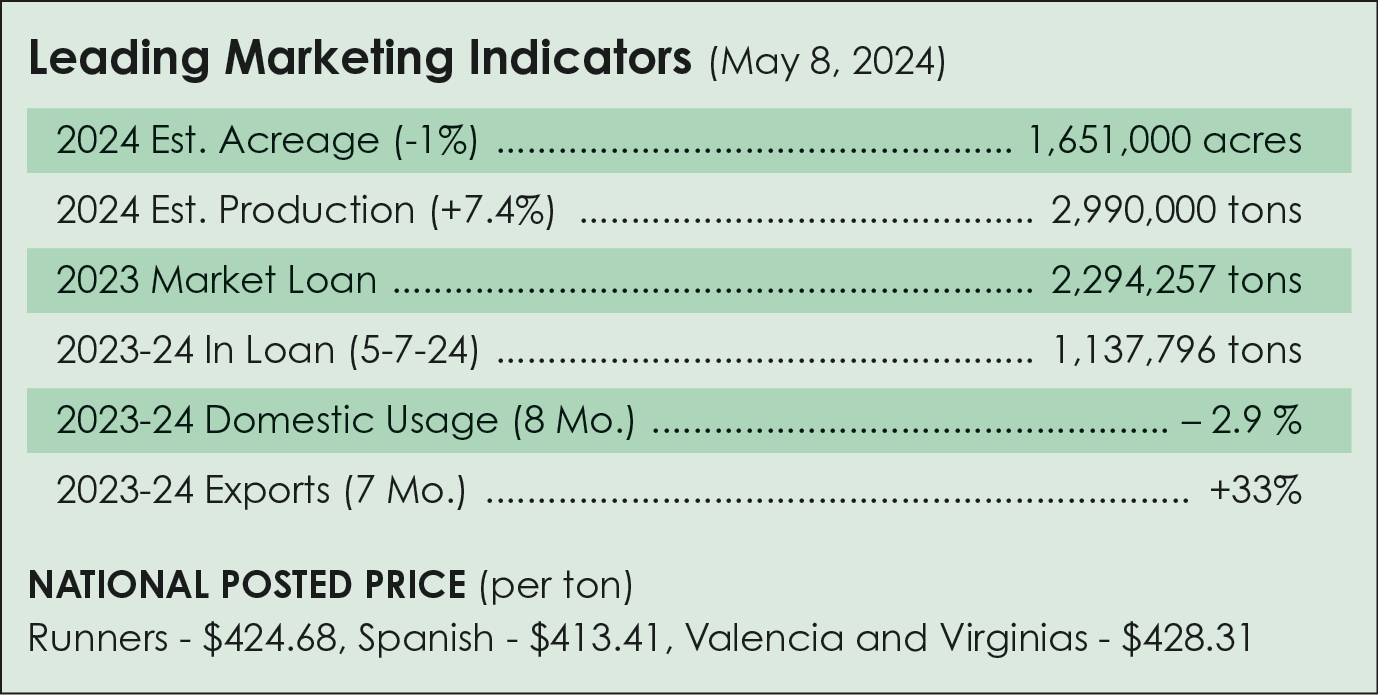

The U.S. Department of Agriculture says farmers intend to plant 6,000 more acres than last year for a total of 1.65 million. Farmers in Georgia and Alabama, the two top producing states, are expected to plant 50,000 more acres in 2024 compared with the prior year.

Farmers in Texas report intentions to plant 65,000 fewer acres than last year. Smaller states like Missouri, Florida and South Carolina intend to increase their respective peanut planted areas, offsetting the loss of acres in Texas. However, some growers were not in agreement with USDA’s numbers and that Texas’ decline would be offset and then some.

The first USDA planted crop estimate had acreage down 1% with continued problems with Texas’ drought. Meanwhile, on the 7% increase in the Southeast, most agreed this would not flood the market, but if harvest was abundant, the carryforward would steady the market.

Production Estimates

USDA is estimating a production of 2.9 million tons. Total peanuts available for the market are 4,008,500 tons. Markets for disappearance are domestic food, crush, exports and seed/residual for a total of 3,031,500 tons. Ending stocks could drop 4% to 977,000 tons. Domestic food usage has declined 0.6%, with exports increasing 21% to 725,000 tons.

Contracts are not likely to be offered again until certified or reported peanut acreage is posted by the Farm Service Agency one month after the July 15 deadline. Shellers are not likely to offer lower shelled prices until they get a more accurate accounting of crop tonnage.

Meanwhile, other storm clouds could impact progress. No. 1 is weather. Texas continues to miss rains in the Southwest, while floods and storms are mangling other areas. The Southeast has received early rains to get the crop off to a good start, but more will be needed by pegging time.

Domestic Markets

Another factor that bothers industry leaders is the sudden drop in domestic consumption. USDA’s utilization charts show a 3% decline from this past year. An eight-month comparison saw peanut usage in candy down 2.5%, peanut snacks down 13% and peanut butter down 0.4%…all leading to a decline of 2.9%.

The cause seems to be inflation, which has most all food items costing much more. The cost of food ingredients has also increased to manufacturers, and that includes peanuts and peanut butter.

Export Markets

Export demand for U.S. peanuts is tightening the supply before the 2024 peanut crop can be grown and warehoused. With four months remaining in the year, the industry could reach the USDA estimate of 725,000 metric tons farmer stock. The top two markets continue strong with 25% volume going to Mexico and 22% to Canada. The American Peanut Council export team made major accomplishments in The Netherlands (+318%) and the United Kingdom (+135%).

More than 85% of U.S. peanut exports currently go to mature markets. The next step change will need to come from new categories in existing geographies or new geographic markets. Shipments are up 21% over last year.

Growth in total peanut kernel imports by Mexico has slowed, but peanut butter consumption is still nascent. Peanut butter also appears to be driving European and United Kingdom peanut consumption growth.

In Argentina, the current crop looks good, and USDA forecasts production at 1.35 million metric tons in both 2023/24 and the next harvest on 400,000 acres. Yields are expected to average in the range of 3.4 to 3.5 tons per hectare. Recent high humidity, coupled with drizzle, have slowed harvest.

Farm Bill

Peanut leaders are planning on a Farm Bill this year that includes a reference price increase and base acres for new growers.

Keep the faith. As one commentator said this week, “peanuts are medicine.” That’s quite a compliment for the humble peanut!

{kind=link}