⋅ BY BOB PARKER ⋅

I believe the peanut industry has a unique opportunity to participate more fully in the peanut oil market. We are saddled with a carryout of almost 1.2 million tons versus production of 3.1 million tons or 38% of production. Meanwhile, we are importing the equivalent of about 40,000 farmer-stock tons of peanut oil. Something’s wrong with this picture.

We are also struggling to hold onto China as a major export market. In 2020, we exported over 800,000 FST of peanuts, 389,000 tons of that to China. USDA projects we will only export 600,000 tons this year and 625,000 tons next year. Based on shipments, we will be fortunate if China buys 125,000 tons in 2022. I believe if we had more peanuts suitable for oil production, China would be at our doorstep.

Why Dedicate A Portion Of Production To Peanut Oil?

The United States consistently grows 3 million tons or larger crops. Unfortunately, it’s difficult to consistently find markets. We need to look at how to balance production with what markets are looking for, whether it is edible or for crushing to produce oil and meal, domestically and internationally. That may mean producing fewer edible peanuts and more for oil.

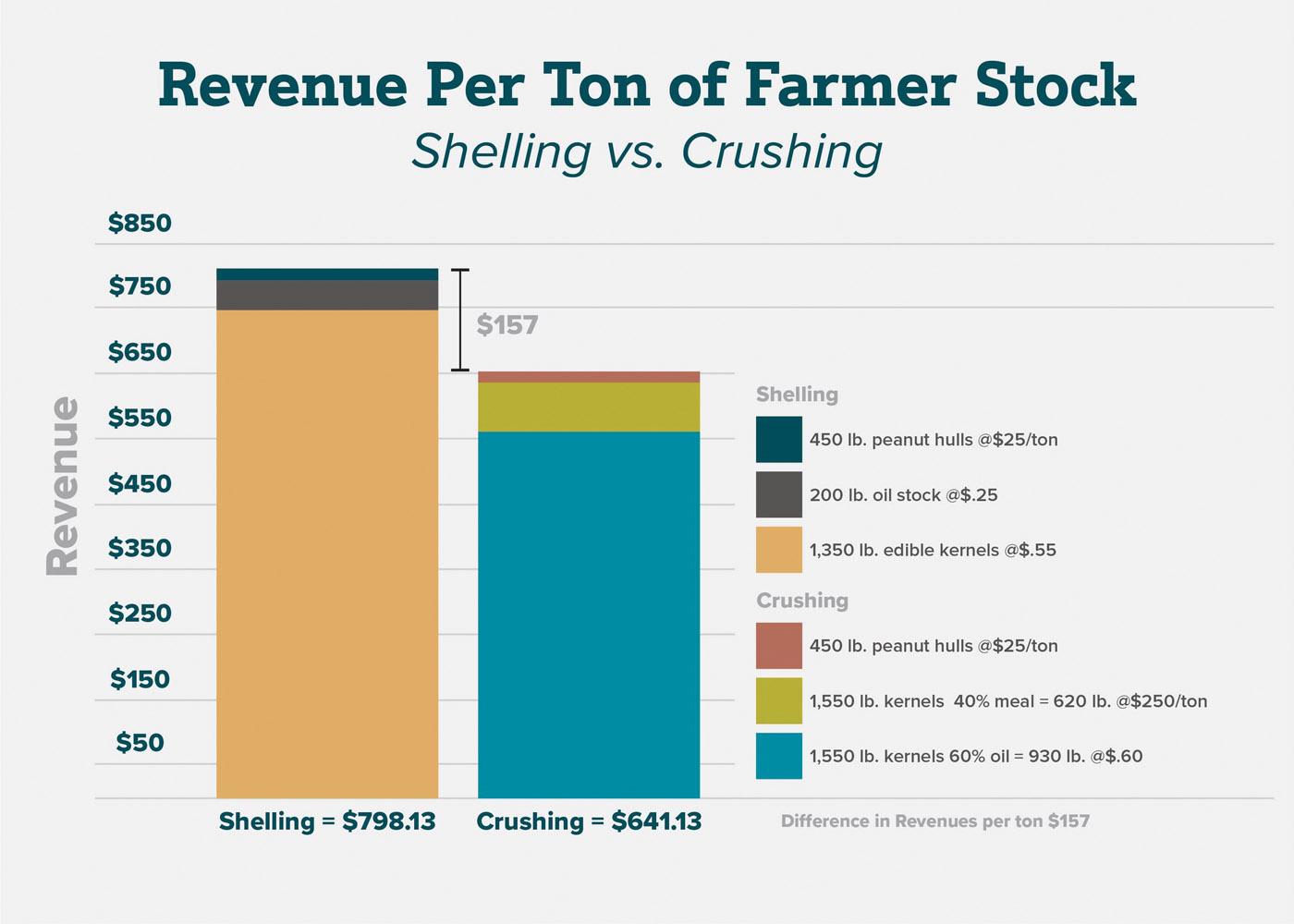

There is demand at home for peanut oil, as well as in international markets, such as China and one day, India. However, to make it work, we must address inefficiencies that make it hard to compete with other peanut oil origins; and tap into genetics to produce varieties with higher oil content suited especially for oil.

U.S. Participation In Peanut Oil Markets

Global production of peanuts runs approximately 50 million metric tons per year. The USDA’s Foreign Ag Service’s World Oilseeds Report predicts 50.5 MMT of production this year. The report shows the world crushes about 20 MMT of peanuts for oil each year, which is slightly less than 40%, and produces 6.29 MMT of oil per year. In recent years, the U.S. has produced about 5% of the world’s peanuts, yet we have averaged only 1.8% or 115,599 metric tons of oil production. We are not servicing an important market at home and internationally.

Our best export year was 2020 at 805,000 FST. Because of the poor-quality crop in 2019, shellers had low-quality peanuts to sell. China bought 389,000 FST to meet their oil need. The 2021 crop will be reserved for edible use. These peanuts are too expensive for China to use as oil, and they will look elsewhere.

In Summary

The U.S. peanut market is extremely mature; 94% of American homes have at least one jar of peanut butter. Only modest rates of growth come from record levels of per capita consumption. Without significant exports, we do not have demand to justify growing 3-million-ton crops yearly. Segmenting part of our production to peanut oil would allow us to supply our domestic needs and make us more competitive in the international market.

The numbers must work for all parties. Efficiencies can be achieved in growing, handling and processing to make it feasible. To do so requires some bold steps and innovative thinking from farmers, breeders, economists, engineers and processors.

{kind=link}