Contributing Editor

Midway through the 2022 peanut harvest, farmers are disappointed and worried about the future.

Tomato Spotted Wilt Virus was more prevalent this season than in the past decade. Rains were feast or famine in many areas, and at one point, harvest of dryland acres had almost shutdown until it rained.

The worry is how much this crop will cost and if there will be a profit when it’s over. Disease and insect pressure are present. Lower-than-expected grades and reduced yields chip away at any profits.

Market Movement

Although the U.S. peanut market remains relatively quiet, farmer stock offers jumped to $600 per ton for uncontracted tonnage. Most farmers had settled for $500 to $550 per ton in the spring as financial lenders wanted something on the books. The Virginia-Carolina region had supported $600 to $625 per ton early on.

Price Loss Coverage payments are made when the market year average is below the reference price. Payments are made in October. The market year average is based on the average prices paid to farmers for the past year (Aug. 2021 to July 2022). The peanut market year average for this period was 24 cents per pound or $486 per ton.

The effective reference price for peanut is 27 cents per pound or $535 per ton. The higher of the loan rate (18 cents per pound or $355 per ton) or market price average ($486 per ton) is deducted from the reference price ($575 per ton). This equals a PLC payment of $49 per ton. This payment is applied to 85% of the peanut farm base. The U.S. Department of Agriculture Farm Service Agency will have verified prices and begun making a payment to farmers last month.

Production

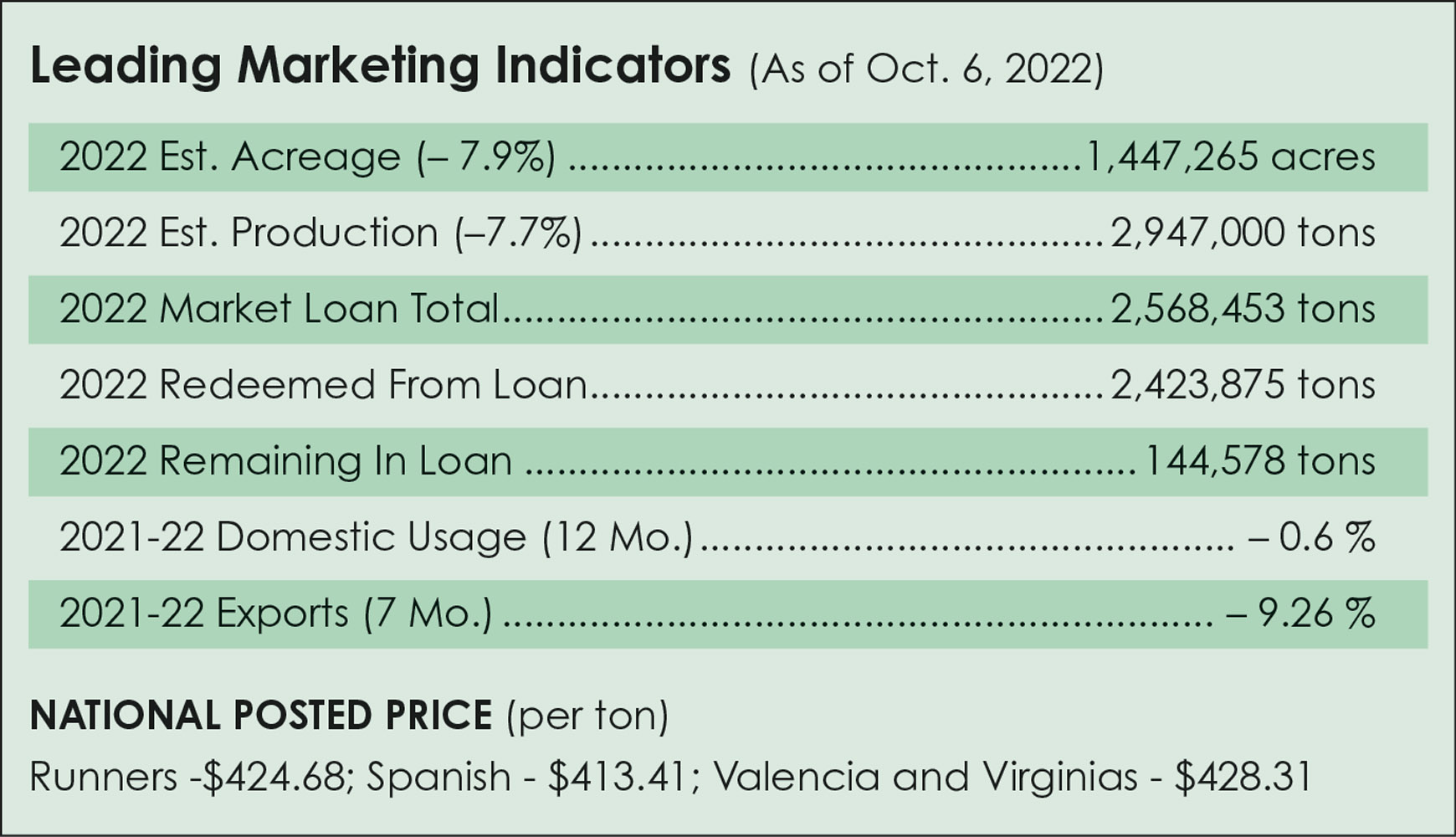

USDA estimated the crop at 2.9 million tons in 2022, down 6% from the previous forecast and down 8% from 2021. Planted area at 1.46 million acres is down 8% from 2021. Area harvested is expected to total 1.41 million acres, down 6% from the previous forecast and down 9% from 2021.

Total average yield across the United States is forecast at 4,145 pounds per acre, up 16 pounds per acre from the previous forecast and up 10 pounds per acre from 2021. Record-high yields are forecast in Florida, North Carolina, South Carolina and Virginia. These estimates were made in September before Hurricane Ian and, therefore, could be lower in October.

The year-long drought in the Southwest will increase abandoned acres, plus officials estimate that at least 40% of the Texas crop will see a big yield loss. Virginia has hit a dry spell just before harvest. Nationwide, drought has affected much of the 2022 crop.

Domestic Markets

Peanut usage for the 12-month period from August 2021 to July 2022 is down only 0.6%. Peanut butter dropped 4.2% for July and is down 2.7% for the year. Candy was up 13.1% for the year, while snack peanuts showed a 4% decrease.

The National Peanut Board tracks consumer trends and reports that taste, price and familiarity continue to drive consumer purchases. Another trend is consumers’ concern regarding their individual food and beverage choices impact on the environment. How the food impacts their health is still important, and snacking throughout the day has been an increasing habit. Peanuts and peanut butter are winners in these trends.

Export Markets

Peanut exports are down 9.3% January thru July 2022. Mexico and Canada continue to make major purchases. China’s purchases have declined during this period by 45% compared to last year. For other nations, the buying trend is good. During this seven-month stretch and compared to the same time one year ago, major buyers include The Netherlands (up 17%), Germany (up 53%), Japan (up 23%) and South Korea (up 75%).

The Chinese are buying from Argentina and Brazil for oil production. Prices for raw-shelled peanuts keeps inching higher. Chinese production has been hit with extreme weather, and the result on this market is unknown. Harvest in China occurs about the same time as in the United States.

Argentine prices are higher amid a reduction in acreage and because of drought. Brazil’s peanut production is growing and becoming a major player.

Looking Ahead

What about plans for peanuts in 2023? With cotton and corn at record levels last season, farmers were willing to delay some contracting and take that risk. It paid off this time with higher contract offers later. Production costs and inflation will influence farmers decisions on which crop to plant next season. With acreage cut 8% and fewer peanuts produced plus higher costs of inputs, the market for peanuts next season is anyone’s guess. PG

{kind=link}