University of Georgia agricultural economists offer the ‘2025 Georgia Ag Forecast Peanut Situation And Outlook.’

The year 2024 brought unique challenges for peanut producers across the United States. In Georgia, the season began with delays because of a wet spring, followed by hot and dry conditions during the early and late summer months. Hurricanes Debby and Helene disrupted key peanut-producing regions, creating further complications. Despite these obstacles, the U.S. peanut production forecast for 2024 is 2.95 million metric tons, an increase of 10.8% compared to 2023. This marks the third-largest peanut production in U.S. history, trailing only the record years of 2017 and 2012.

This significant production highlights the resilience and adaptability of American peanut farmers. The United States is the fourth-largest peanut-producing country in the world in 2024, after China, India and Nigeria. In 2024, Georgia and other peanut-producing states expanded peanut acreage as lower relative prices for cotton, corn and soybeans made peanuts a more attractive option.

Average Yield Decline

Nationwide, planted peanut acreage increased by 9.7% from 2023, reaching 1.8 million acres — the second-largest total in the past decade, following 2017. Harvested acreage is estimated at 1.75 million acres, slightly below the planted acreage. Georgia growers, in particular, expanded their peanut acreage from 775,000 acres in 2023 to 850,000 acres in 2024, which is 47% of total U.S.-planted acres.

The 2024 peanut crop yield is forecast at 3,723 pounds per acre, representing a 1.4% decrease from the 2023 average yield of 3,775 pounds per acre and falling below the five-year average of 3,938 pounds per acre. The decline in yield is primarily attributed to the impact of Hurricane Helene on peanut farms in Florida, Georgia and South Carolina.

Despite the yield challenges, the overall quality of the 2024 peanut crop is excellent. According to the Georgia Federal-State Inspection Service, as of Dec. 13, 2024, 99.5% of the crop is classified as Segregation 1, the highest grade used for the edible market. Segregation 2 is 0.4% and Segregation 3 is just 0.1%, which is unsuitable for the edible market but can be used for crushing peanut oil. These results highlight the production of a high-quality crop with minimal damage or aflatoxin presence in 2024.

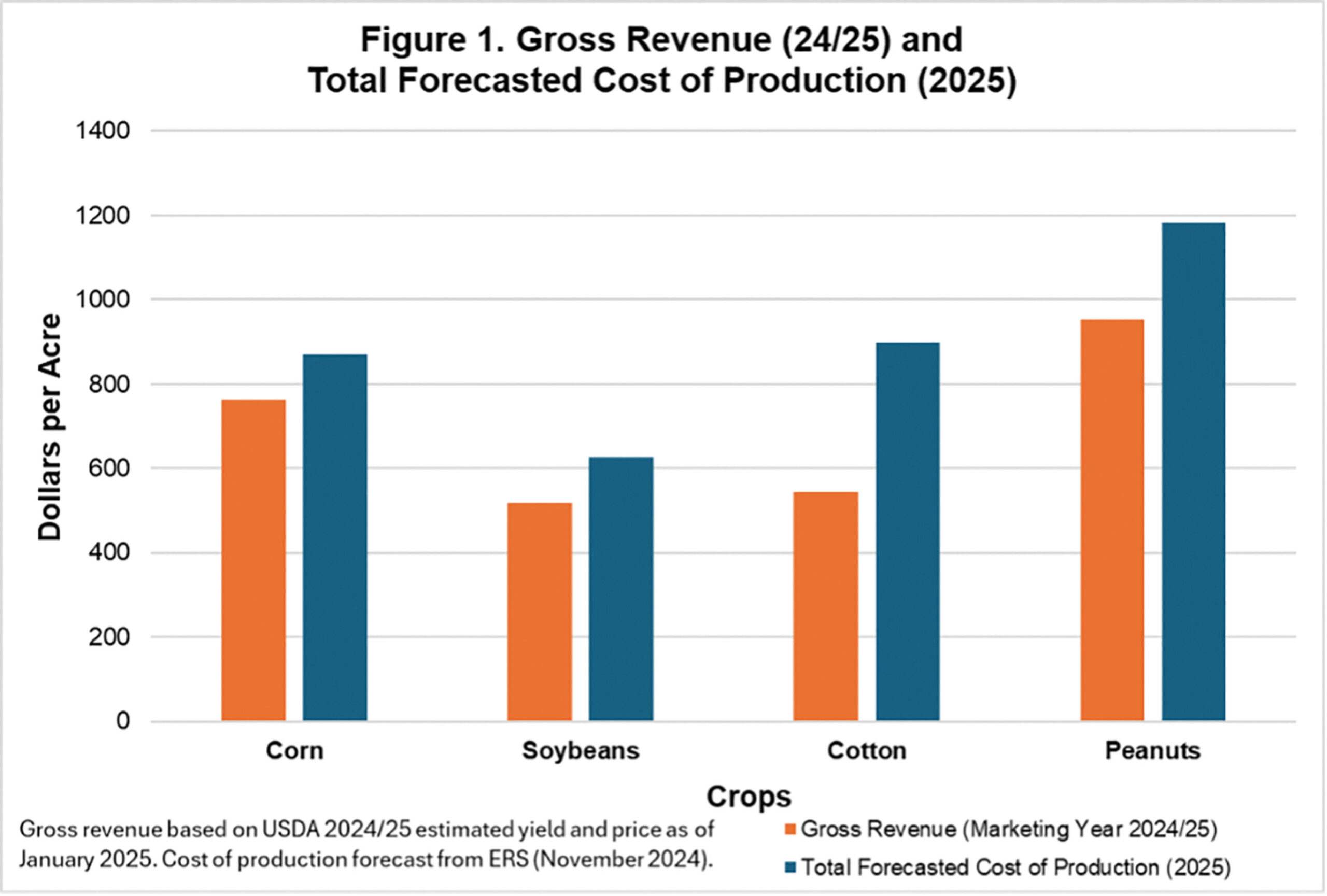

Using Cost Of Production Forecasts To Assist In Marketing

Knowing the expected cost of production is essential for developing effective risk management and marketing strategies. At an aggregate level, forecasts of costs provided by the USDA Economic Research Service can offer a useful benchmark to help understand the gross revenue and cost of production for commodities at the national or regional level. These forecasts can be used to determine breakeven prices to inform a risk management and marketing plan.

The ERS’s 2025 national cost of production forecast for major southern row crops: cotton, peanuts, corn and soybeans, indicates a decline in fertilizer and interest costs, contributing to lower total operating costs for most crops compared to 2024, except cotton. However, rising custom rates, other variable expenses and allocated overhead costs offset some of these savings, resulting in an expected total cost of production that is effectively the same as the estimated 2024 cost of production. Peanuts have the highest forecasted total cost per acre ($1,181.84), followed by cotton ($899.96), corn ($871.09) and soybeans ($624.77), highlighting the significant investment in producing Southern row crops. It is important to note that these forecasts were released by the ERS in November of 2024, before tariff threats were made, that if implemented, may increase costs of some agricultural inputs, notably fertilizer.

At the currently forecasted cost of production, the negative returns experienced by row-crop producers in 2024 are expected to remain a major concern for all four crops in 2025 if prices do not improve.

Determine Your Breakeven Price

Whether yields can provide increased revenue is a question for the future, but given national corn yields in 2024/25 being estimated at record levels and soybean yields being estimated at about 2% below record levels, it is more likely that price is going to be the primary driver to increase revenue for these crops. Meanwhile, multiple weather events made a major impact on cotton yields that were about 12% below record levels and peanut yields that were about 11% below record levels. Therefore, some of the shortfall in revenue for cotton and peanuts could come from higher yields.

The other component of the revenue equation is price. Determining a breakeven price assists in making informed decisions about the price necessary to cover production costs. To determine a breakeven price, divide the forecasted cost of production by expected yield. At the current national forecasted cost of production and average yield for the last five years, the breakeven price for corn and peanuts would have to increase 17% over the estimated 2024/25 price. For soybeans, the price would have to increase 21%, while cotton prices would have to rise 59%.

Ultimately, the actual cost of production varies among individual farms, as it depends on many factors such as economies of size and scope, relationships with input suppliers and adopted management practices. Actual yields also vary, and thus, producers need to consider their own potential breakeven price. Repeating this exercise for a specific farm can be helpful in planning, making risk management and marketing decisions and finding potential opportunities to make efficiency improvements to reduce costs for the upcoming crop year. PG

Article by Adam Rabinowitz, Auburn University Associate Professor, Agricultural Economics & Rural Sociology.

Consumption Levels Off From Pandemic High

The total peanut supply for the 2024–25 marketing year consists of three key components: carryover stocks from the 2023 crop totaling 672,000 metric tons, the 2024 production forecast of 2,954,000 metric tons and 45,000 metric tons of imports. Together, this brings the total supply to an estimated 3,671,000 metric tons. Total U.S. peanut use for the 2024 crop is projected to be slightly below that of the 2023 crop but remains at a relatively high level. The total disappearance of peanuts — including food consumption, crushing, exports, seed use, shrinkage and residual — is forecasted at 2,924,000 metric tons. This will leave an ending stock of 747,000 metric tons for the 2024–25 marketing year.

Per capita peanut consumption reached a record high of 7.6 pounds during the pandemic but has since leveled off with a slight decline. In 2023, per capita peanut consumption was estimated at 7.2 pounds. According to the U.S. Department of Agriculture’s Peanut Stocks and Processing report released on Nov. 25, 2024, shelled edible-grade utilization for the season to date (August–October 2024) totaled 596,926,000 pounds, a 3.8% decline compared to the same period last year. Within this category, peanut butter remains the largest use of shelled peanuts, followed by peanut snacks and peanut candy. Peanut butter consumption has fallen by 4.8%, peanut snacks have increased by 2.2% and peanut candy usage has decreased by 7.2%. These shifts are largely attributed to the current economic climate, which is influencing consumer demand for peanut products.

While most peanuts produced in the United States are consumed domestically, we are the fourth-largest peanut exporting country in the world, after India, Argentina and China. U.S. peanut exports account for approximately 22% of total U.S. production, representing about 14% of the global peanut export market share. The top five export destinations for U.S. peanuts are Mexico, Canada, China, the Netherlands and the United Kingdom. However, trade policy uncertainties could pose challenges for U.S. peanut exports, potentially limiting market opportunities and exerting downward pressure on peanut prices.

Looking ahead to 2025, carryover stocks are projected to be approximately 747,000 metric tons. With low cotton prices, shellers are in no hurry to offer contracts or purchase peanut acreage. Additionally, persistently high fertilizer costs may incentivize farmers to continue planting peanuts. Considering these factors, it is reasonable to anticipate lower-priced forward contracts compared to 2024. For Georgia growers, season average prices are expected to range between $475 and $525 per ton. If these price levels are realized, peanut profitability will remain a significant challenge for producers in 2025.

To view the Georgia Ag Forecast webinars and download the full report, go to agforecast.caes.uga.edu/webinar-recordings.html. PG

{kind=link}