Contributing Editor

The peanut market is trending higher on extremely thin trading. Current raw-shelled peanuts are available in the high 50s. With all of the uncertainty in the economy and questions about the 2022 crop, shellers are not rushing to make a sale until more facts surface in the market. So, the market remains quiet with only sales on small orders.

On new crop, shellers are uninterested as many farmers are unwilling to contract farmer-stock peanuts as they study offers for cotton. Any sheller sales for new crop would have to be 60 cents plus. The talk in the trade is that late/delayed final peanut plantings for new crop are anticipated to be 8% to 10% less this year as some farmers planting late have planted cotton. Buyers/sellers want to watch markets for a while to judge progress of this new crop and weather development before making future decisions.

Late Planting Affects Acreage

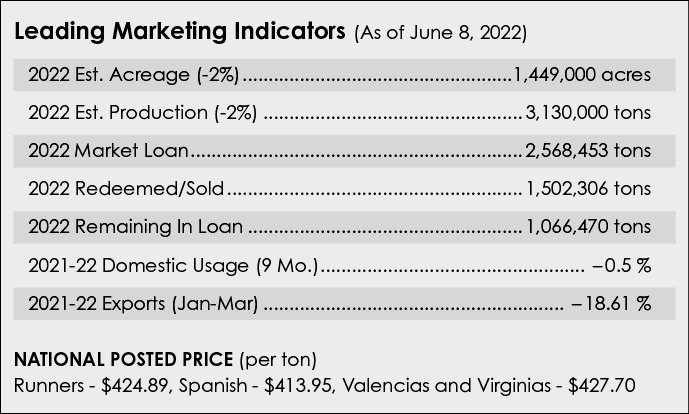

An updated prediction is that U.S. peanut production is forecast this year to be 3.1 million tons, a 2% decrease. Harvested acres are estimated at 1.5 million acres, down 2.4% from last year. Earlier estimates had acreage down 1%. The U.S. average yield is forecast to be 4,151 pounds per acre, a 3.9% increase over last year.

Market demand or disappearance is estimated to be 3.19 million tons, a 4% increase. Domestic food use is forecast up 1.4%. Crushing for oil is about the same with exports remaining at 625,000 tons. Ending stocks will drop slightly to 1.15 million tons.

There is a lot of uncertainty over the planted area. The market consensus is that the original U.S. Department of Agriculture prospective plantings estimate is inflated. Market participants expect that the actual decrease in planted area will be upwards of 5%. Another analyst said he wouldn’t be surprised to see plantings closer to 10% down from last season. Prices for alternative crops such as cotton and corn are at elevated levels, while peanut prices have remained relatively flat over the same period.

Returns Not Easy To Figure

With crop insurance deadlines approaching, producers had to make a decision. Cost of production, especially fuel, and inflation were factors to consider. One sheller has announced a new program that will give growers an annual payout in addition to their regular option payment. This program will be in effect every year going forward.

To start, the company will offer a bonus to all producers who deliver to their buying points. The first payment in the fourth quarter is at least $20 per ton. That is on top of any market base contracts. The company will pay back the bonus against eligible tons, which is the three-year rolling average delivered per entity. Return is based on financial performance of the total peanut business. Current crop tonnage must be contracted for the return to be released by Dec. 31.

The expansion of cooperatives and the price increases for raw-shelled peanuts make estimating farmer returns per ton difficult. Shellers have minimum loan contracts with pool payments as early as October. The average price of peanuts has been pushed only slightly higher this year and is estimated by USDA at $484 per ton average. Subtract the average price from reference price of $535 per ton and that yields a price loss coverage payment of $51 per ton in October for the previous year.

Domestic Markets

For the domestic market, USDA is reporting peanut usage down .5% for the nine-month period for raw-shelled peanuts in primary products. Peanut butter is down 1.9%, with an April 2021 versus April 2022 comparison down 3.3%. Candy is still up 15.4% for the nine-month period but was down 0.4% in April. Snacks are down 5.2%. A nationwide recall for salmonella, plus summer travel, have led to a sluggish market.

Export Markets

For the export market, USDA reports that it is down 18.61% to 322,679 metric tons for January, February and March, compared to the same three-month period of last year. The top buyer was Mexico with 32,824 metric tons, up 5.83% from last year. Canada was second with 30,890 metric tons, up 2.62%. Other top buyers were The Netherlands, Japan and the United Kingdom.

China has reduced purchases of U.S. peanuts to 23,397 metric tons, down 59.7% from the same three-month period last year. China needs more peanuts for peanut oil, but U.S. peanuts may be too expensive as China is considering India.

The peanut industry is doing well in spite of war, inflation, immigration, lack of labor, fuel and gas costs and government regulations that hurt farmers. Strategic management during these trying times will be the difference.

Peanuts and peanut butter are great products that are nutritious, fun to eat, a good fit for today’s lifestyle, affordable, available and sustainable.

{kind=link}