Contributing Editor

The unknowns in agriculture have cast a cloud of doubt over plans a farmer makes for the next season. As planting time arrives, the unknowns turn into surprises. Costs have increased as he or she orders fertilizer, chemicals and gypsum. Repairs on old equipment will be required as new purchases will have to wait. Market prices for most commodities are at or below the cost of production.

Meanwhile, foreign and domestic markets are showing a significant decline in volume. Although President Trump promises to protect “his farmers,” the impact of tariffs on all commodities is another unknown. As comedian Jerry Clower used to say, “Just shoot up in here, we got to have some relief.”

No Competition For Peanuts

The U.S. Department of Agriculture report was not a huge surprise; however, seeing nearly 1 million acres expected to be planted in Georgia and nearly 2 million peanut acres across the United States is a bit staggering. Unfortunately for growers, there just isn’t enough competition for peanuts that can be planted profitably.

Cotton continues to trade in the high 60 cents per pound for December 2025 delivery. The fact that cotton acres are projected down 12% is in line with industry expectations. With corn under $5 a bushel, it’s easy to see why peanuts are the pick of the litter. Unfortunately for all involved, it’s not a very attractive scenario.

New crop kernel prices are being indicated in the mid-50 cents per pound for Southeast runners, and 70 to 71 cents per pound for Southeast blanched jumbo runners. Buyers have taken on some coverage for 2026, and knowing that we are about to plant a big crop, they are very content to sit back and wait to see what happens at planting and during the growing season before layering in additional tons.

No Guarantee For Two Tons

Growing conditions and weather will be the market maker once again this year. Overall, average U.S. yields have decreased each year since 2021, and it’s probably no longer realistic to assume two ton per-acre yields will be realized. Rotations have been shortened, and many growers are simply in survival mode. How this impacts growers’ ability to apply proper inputs to the crop remains to be seen. If the weather does cooperate, there will be gracious plenty of peanuts to go around come harvest.

A group of dedicated rural Congressional leaders have pleaded that farmers were in trouble and passed the Emergency Commodity Assistance Program, which will use up to $10 billion to issue one-time economic assistance payments to eligible producers for the 2024 crop year. These payments are intended to help farmers cope with losses from natural disasters and a difficult farm economy and will help preserve family farms and ranches across the country while also continuing to ensure food and agricultural security for our nation. For peanuts, the program paid $75.51 per acre on planted 2024 acres.

Ending Stocks To Cover Next Year

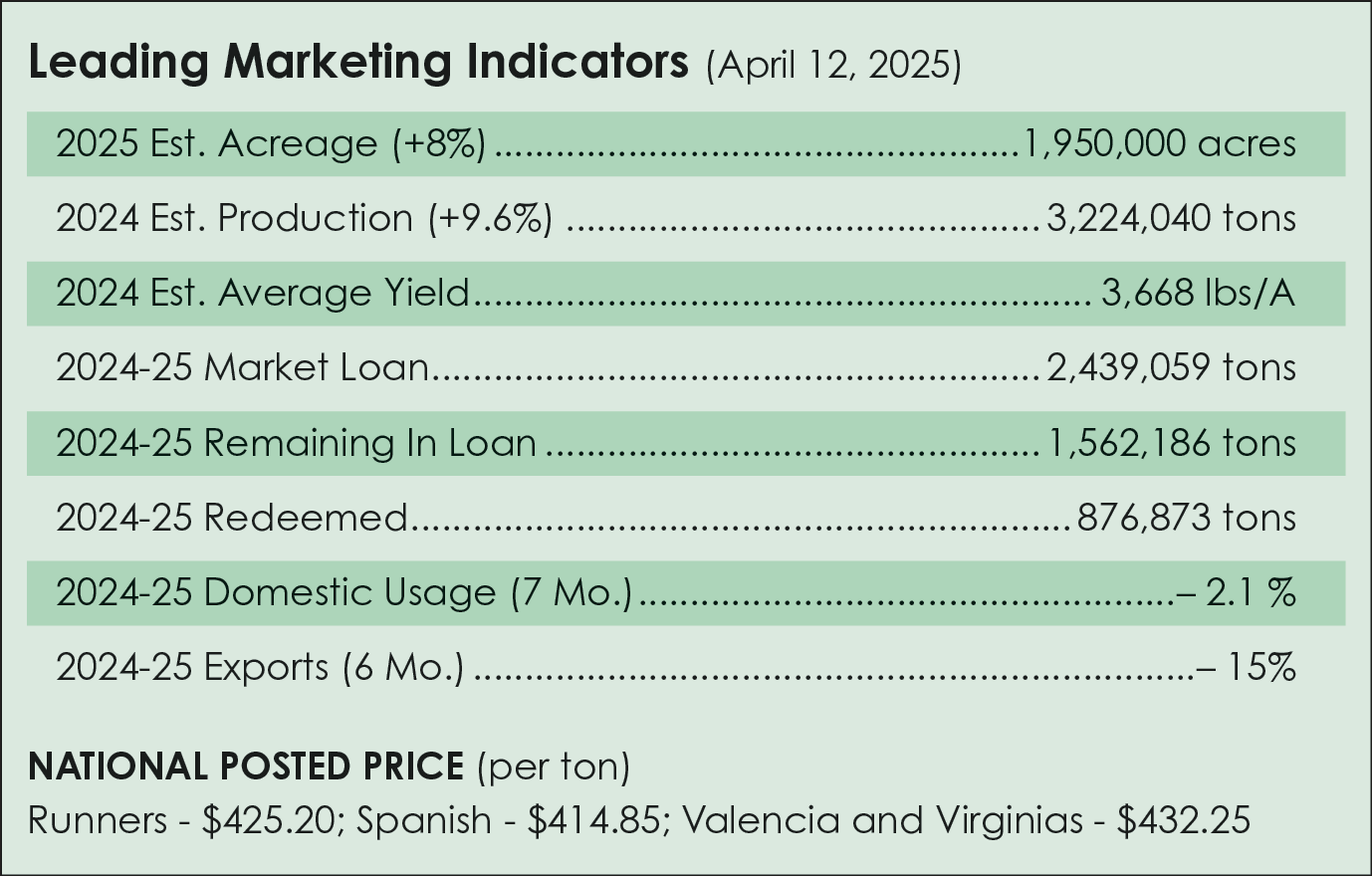

There’s lots of speculation about how many acres will be planted in peanuts for the 2025 growing season and to what effect that will have on both the current- and new-crop markets. In short, we have adequate supply but not a burdensome carry-out come August. Growers intend to plant 1.95 million acres in 2025, up 8% from 2024. Compared with last year, planted acreage is expected to increase 9% or more in Florida, Georgia, Mississippi and South Carolina. In Georgia, the largest peanut-producing state, planted area is expected to be up 12% from last year to 950,000 acres.

A 1,950,000-acre crop averaging 3,881 pounds per acre, the five-year average, would be 3,784,000 tons in total production. The market’s domestic demand is 1,550,000 tons with export demand at 600,000 tons, that’s 2,150,000 leaving an ending stock of 1,634,000 tons, enough to fill the domestic market next year.

Domestic Decline

Raw peanuts in primary products are down 2.1% in August to February compared to the same seven months of 2023. Peanut butter usage dropped 6.3%, pushing the seven-month volume down 2.5%. Peanut candy usage is down 9.4% for the seven months after a 20% decline in February versus last year. Peanuts in snacks are up 0.2% for the past year and now up 4.0% for the seven months.

Contracts for runner-type peanuts opened for $500 per ton in the Southeast. The contract is limited to half of the farmer’s production in 2024. Shellers are reportedly matching the offer if the farmer is ready to sign. Most farmers need contracts to secure financing for the new season. Buying points reported good response. In the Virginia-Carolina region, irrigated Virginias were $605 per ton with non-irrigated at $580 per ton. High-oleic runners were as high as $550 per ton.

Foreign Competition And Export Markets

In addition to this expected increase in U.S. acres, Argentina and Brazil increased acres and have begun to harvest their crop. Argentina should have a good crop for the second consecutive year; however, an early season frost will delay maturity and cause some quality issues that could open the door for U.S. sales.

The President has announced a range of tariffs on all countries and all goods. Those countries targeted with tariffs higher than 10%, for example 20% for the European Union and 24% for Japan, are being delayed until July 9, to allow negotiations to occur between the United States and individual countries. Predicting export volumes is impossible with all the unknowns, but USDA expects a decline of 18%. In increasing promotion funds for the peanut industry, USDA hopes to expand export demand.

With all the unknowns, the suggestion is to negotiate your best price with your local buying point. Plant about the same as last year, stay with your rotation plan, look for chemical and fertilizer deals, pray for a Farm Bill this year and pray for rain.

{kind=link}