The U.S. peanut industry must solve the problem of aflatoxin and change perceptions about quality.

⋅ By Amanda Huber ⋅

For the second year in a row, per capita peanut consumption achieved new levels the National Peanut Board reported in late 2021. Based on USDA and U.S. Census data, per capita peanut consumption has risen to an all-time high of 7.9 pounds in 2021. This tops the previous record of 7.6 pounds in 2020 and reflects an increase of 3%.

The NPB works diligently to promote peanut consumption and has made significant strides toward solving the allergy problem. So, this is good news; however, it was a time when most of the country was eating at home instead of dining out.

At the South Carolina peanut grower’s meeting in late January, Premium Peanut CEO Karl Zimmer says it is okay to look at individual numbers, but he and other industry analysts tend to look more at trends.

“We are growing more than we consume,” Zimmer says. “Peanut farming gets more productive, but domestic demand has not grown at the same rate. At about 1% a year, it is positive, but not keeping up.”

A Look At 2021

Zimmer spoke following Dell Cotton, manager of the Peanut Growers Cooperative Marketing Association. Cotton gave a recap of 2021 acreage, yield and production.

“Acreage in the Southeast has been steady the past two to three years, with each between 1 million to 1.1 million acres,” says Cotton.

The Southwest was down 10,000 acres in 2021 to 224,850. The Virginia-Carolina region had 210,000 acres, down only 2,000 from 2020. Across the three regions, the total was 1.546 million acres.

In the yield category, the Southeast was over the 4,000-pound mark at 4,156 pounds per acre on average. Georgia led with 4,450 pounds per acre, followed by Mississippi with 4,200 pounds per acre.

“In the V-C region, the average yield was 4,349 pounds per acre and that is 150 pounds more than ever before. It was the highest ever yield on average,” says Cotton.

“Three of the past five years, the average yield has been more than 4,000 pounds per acre for the V-C, with 2021 being the highest. Virginia also had a record average yield at 4,700 pounds per acre.”

The Southwest now includes Arkansas, which averaged 5,000 pounds per acre. Oklahoma brought in 4,400 pounds per acre, and the Southwest averaged 3,823 pounds per acre overall.

Cotton says total production was 3.1 million tons of peanuts. A breakdown by market type finds 2.67 million tons of runners and 408,676 tons of Virginias. Domestic demand is estimated at 2.9 million tons.

Challenges In The Export Market

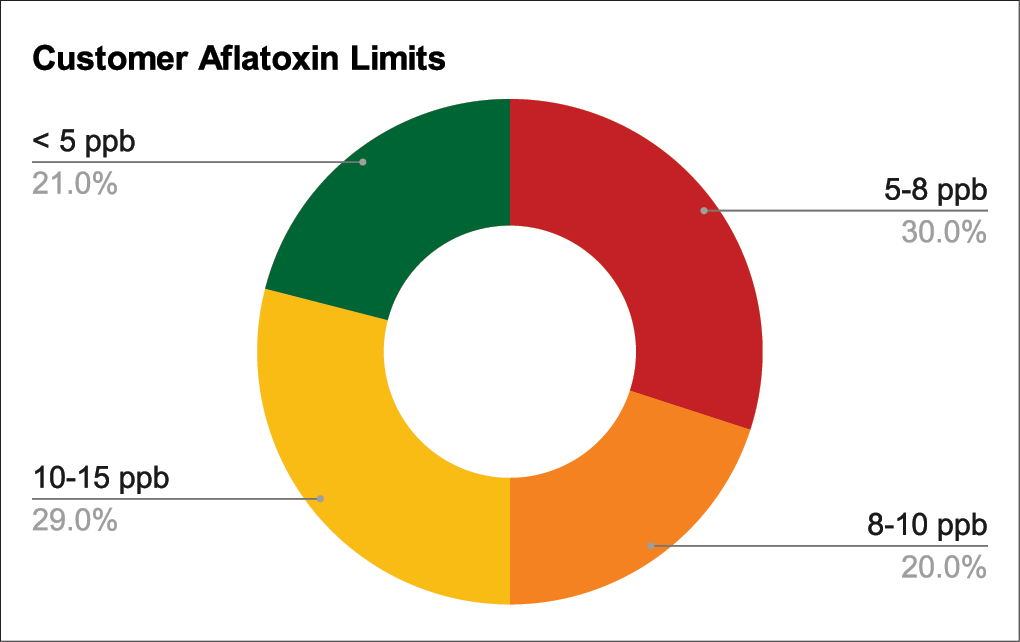

• 71% of customers for U.S. peanuts, both domestically and internationally, have specifications less than 10 parts per billion.

• Many customers require multiple tests with all tests under that standard and/or testing of adjacent lots.

• Codex, the United Nations and other customers are now ordering additional regulations.

• U.S. peanuts are no longer the preferred product internationally, primarily because of the perception of quality.

Exporting The Excess

What about the export market to take up the excess production?

“As an industry, we have done a good job in increasing exports over the previous three years,” Zimmer says. “This past year will be down, but the previous three years, it went up.”

With exports increasing and going to more than 30 countries around the world every year, this could be considered a success.

“Or is it?” he says. “When you look at the price per pound for exports over those three years, exports went up, but the amount collectively that we are getting paid for our product has gone down every year. This highlights a challenge we have as an industry.”

Volume Up, Price Down

“We need to grow exports,” Zimmer says, “but we need to get paid for those exports and the reality is, unfortunately, this is not a good trend. We are exporting more but getting paid less.”

Zimmer says China drives export volume.

“We can look at every other market in the world, Mexico, Canada, Europe and Japan – all important markets, but if you want to understand what is happening to supply and demand on peanuts, look at China,” he says. “China grows 10 times the peanuts we do. Still, they are the largest importer in the world and also the largest exporter.”

U.S. peanuts exported to China are destined for their oil market. China, too, uses their own peanuts for their oil market.

“China does have quality product as well,” Zimmer says. “Japan demands the highest-quality peanuts in the world and their main supplier is China. The No. 1 supplier of the highest quality market in the world is not the United States. That’s a problem.”

Peanuts’ Achilles’ Heel

The European market is also one that demands a high-quality product and is willing to pay for it.

Unfortunately, Zimmer says the United States has lost that market to Argentina. “The Europeans want a product we can’t provide.”

Zimmer says, “What drives the market’s pricing? The No. 1 thing is aflatoxin. If you want to know how profitable or unprofitable the peanut industry is in any one year, look at aflatoxin. In my view, it is the single largest threat to the industry.

“As a sheller, we do everything we know how to do to get a peanut to pass inspection. In 2019, 30% could not be sold into the edible market because of aflatoxin. After shelling, after re-cleaning, after we had done everything, we had tons of peanuts that could not pass inspection. That’s why prices went up.

“We could have shipped it to China at a 20% discount, but that doesn’t help,” he says.

“When you look at aflatoxin, 71% of our customers have a limit of 10 parts per billion or less. Ten parts per billion is one kernel out of 23 million. One kernel is all you need to fail the standard.”

A Standard We Can’t Meet

Why does Zimmer say we have lost Europe?

“Their standard is 2 parts per billion. That’s 1/4 of a kernel in a whole truckload,” Zimmer says. “Above 2 parts per billion and they won’t take it. So, for us to be able to grow exports, it comes back to solving the aflatoxin issue as an industry.”

In late November 2020, the American Peanut Council brought all segments together for a peanut quality symposium to discuss aflatoxin.

“It’s a significant issue. How do we fund efforts to mitigate aflatoxin in the short term and solve it in the long term? If we want to continue to grow as an industry, if we want to make money as an industry — the whole industry — we have got to figure out aflatoxin,” Zimmer says.

Bypassing The U.S. Government

Yet another challenge is knowing and understanding the regulations customers are asking of their peanut suppliers.

Zimmer says, “We regularly get surveys from our customers, and it will be a 50-page questionnaire with all these regulations they want us to comply with as a supplier. If you look at the questions carefully, they are asking us to comply with United Nations labor regulations that the United States has not approved because they do not work here.

“One of those regulations is that I certify that no one in my entire supply chain, which includes all of my growers, will have anyone working on the farm under the age of 18, even if they are your own children. That is level of oversight our customers are demanding.

“They can’t get our government to negotiate this. They can’t get our current or former administration to the table to discuss this, so they are bypassing governments and going straight to the companies that want to sell products in the European market. They are forcing you as a seller in the European market to do what no administration will do. That’s what we are faced with. That’s the challenge.”

But it is the perception on quality that Zimmer thinks can be improved.

“I believe as an industry we can change the perception that U.S. peanuts are not the highest quality,” he says. “We can change that if we focus on things like aflatoxin. We can regain markets where they are all willing to pay for the high-quality product that we know we can produce. But we must work together.

“U.S. peanuts are no longer the preferred peanut internationally, but we can solve this.

“We must work together across the supply chain — with seed breeders, growers, buying points, shellers, all segments — to maximize the value of the product because we can change these perceptions.” PG

{kind=link}